Why We Deliberately Chose the Less Glamorous Market

When German investors look at the U.S. real estate market, the same names come up almost every time: New York, Miami, and Los Angeles. International prestige, iconic skylines, and years of price momentum give these markets an appeal that is difficult to dismiss at first glance.

That is precisely why they dominate deal memos, investment presentations, and market conversations. But public visibility is not evidence of investment quality. We examined all three markets rigorously — and excluded all three deliberately.

New York: Regulatory Risk Is Compounding

We rule out New York on regulatory grounds. Political intervention has steadily reshaped the market — at the expense of predictability for property owners. Rent regulation, limited adjustment mechanisms, and a legal environment that affords landlords ever less operational flexibility have fundamentally altered the risk-return profile.

The Good Cause Eviction standard is particularly consequential. In practical terms, it means that a landlord cannot simply allow a lease to expire or terminate a tenancy without a legally recognized reason. More substantial rent increases, meanwhile, can be challenged in court. For property owners, the result is narrower room to maneuver, greater legal uncertainty, and a measurably reduced ability to manage assets actively.

That is the point that matters most for us. A market loses its appeal not only when demand weakens, but when ownership ceases to function as an operationally controllable asset. That is the direction New York is heading.

Los Angeles: More Regulation, Less Flexibility

Los Angeles is excluded for similar reasons — in some respects, even more clearly so. The city overhauled its Rent Stabilization Ordinance (RSO) in 2025. Going forward, permissible annual rent increases will be calculated under a new formula: 90% of average CPI, capped at a range of 1% to 4%. Allowances previously available for certain landlord-paid operating costs have been eliminated.

For investors, the direction is unambiguous: the scope for rent adjustments is being defined more narrowly, while the operational reality on the ownership side is not becoming easier.

Maintenance, insurance, staffing, financing, and regulatory compliance do not move in lockstep with politically constrained rent increases. That divergence is precisely where the economic imbalance originates. Beyond individual rule changes, Los Angeles is signaling a broader policy trajectory. For investors, what matters is not only the current regulatory framework, but whether a market is likely to become more predictable or more restrictive over time. In Los Angeles, the evidence currently favors the latter. Los Angeles County has also enacted a countywide eviction moratorium, adding further regulatory pressure on property owners.

Miami: Strong Brand, Weaker Fundamentals

That leaves Miami — the market with the greatest visibility, the strongest international profile, and arguably the most compelling marketing story. That is precisely what draws many investors in. For us, however, visibility alone is insufficient.

What matters is whether prices, supply, rent trends, and cash flow still align in a defensible way. That is where our skepticism took hold. Miami is not a market we are dismissing from a distance. It is a market we examined closely — and whose fundamentals failed to justify the narrative priced into it.

The Narrative and the Quiet Crisis Beneath It

Miami is currently a textbook example of what happens when capital flows override fundamental analysis. What is taking shape in Brickell and Downtown Miami is no longer a temporary market dislocation — it is a structural imbalance that extends well beyond the condo sector.

Condo Market: Too Much Supply, Too Little Absorption

The Brickell condo market has shifted decisively into buyer’s territory. With roughly 19.3 months of supply on hand, available inventory sits well above what a healthy market equilibrium would suggest — typically six to seven months. At the same time, condo sale prices have declined more than 12% year-over-year, and price per square foot has fallen noticeably.

This is not the signature of a short-term market correction. It reflects the consequences of overcapacity built up over years. Brickell alone already contains approximately 26,500 condo units. An additional 4,500 units are in the pipeline — a further supply increase of roughly 17%. Existing inventory is particularly exposed, forced to compete against newer projects with more modern finishes, stronger amenities, and greater marketability.

Resales are increasingly closing at meaningful discounts to original asking prices. The pattern is visible across Greater Downtown Miami as a whole: nearly 26,100 condos are currently listed for sale, equivalent to 12.9 months of inventory. A market at these levels is no longer driven by scarcity — it is driven by growing internal competitive pressure.

Apartment Market: Record Construction Meets Softening Demand

The apartment segment is more severe still. Early in 2025, Miami recorded 32,014 units under construction — the highest multifamily development activity among the 90 largest U.S. metropolitan areas. That represents a supply increase of 23.8% relative to existing stock, a pace that stands out even by national standards. To put it plainly: Miami alone is delivering more new apartments than Tampa and Jacksonville combined.

That is the core problem. A market can absorb high construction volumes only when demand, absorption, and rent growth remain in balance. In Miami, the evidence increasingly suggests that balance has broken down. Of more than 35,000 units under construction across South Florida, only about 21% have entered pre-leasing or lease-up.

Even within the market itself, participants are openly discussing flat rent growth and an extended adjustment period. This dynamic has been documented in Bisnow’s analysis of Miami’s oversupply and softening rents. For investors, the signal is clear. When supply grows faster than sustainable demand, negotiating leverage shifts. Concessions increase, rent growth decelerates, and new acquisitions become harder to underwrite on defensible operating assumptions.

A Market Under Growing Internal Pressure

Anyone buying in Miami today — whether condo or apartment — is not investing in a market with clear tailwinds. They are investing in a market increasingly weighed down by its own supply dynamics. That is the quiet crisis behind the polished narrative.

From the outside, Miami remains a market defined by brand, momentum, and international appeal. Beneath the surface, the data tells a different story: rising supply pressure, deteriorating price trends, decelerating rent growth, and intensifying competition between existing and new inventory. The result is a central misperception among many investors: Miami looks stronger from the outside than the market actually is from within.

Infrastructure Already at Its Limits — Before the Next Wave of Development Arrives

One factor conspicuously absent from most investment pitches: Miami has a structural infrastructure problem that intensifies with each new tower that breaks ground. According to the INRIX Traffic Scorecard, Miami ranks among the most congested cities in the United States — sixth nationally. For drivers, that translates to an average cost of $1,325 per year in lost time and productivity. For the city as a whole, the economic toll amounts to roughly $3.4 billion annually.

A significant contributor is the weakness of Miami’s transit network relative to its building density. While New York, Los Angeles, and most other major U.S. metros operate substantially larger rail and public transit systems, Miami remains structurally underserved.

The local rail network comprises just two lines and 23 stations. New York City, for comparison, operates 472 stations.

The congestion is most acute in Brickell and Downtown Miami. The corridor around Brickell Avenue and Eighth Street has become a chronic pressure point under continuous monitoring by FDOT and county agencies. Meanwhile, construction of the I-395 Signature Bridge has stretched years beyond its original schedule: completion was initially planned for 2024, pushed to 2027, and now stands at 2029. The project carries a price tag of approximately $860 million — and has functioned as an additional burden on Downtown Miami commuters for years.

That is the deeper problem. The city continues to grow, new residential and apartment projects continue to come to market, but infrastructure relief is not keeping pace with construction. For investors, this is not a secondary concern — it is a genuine fundamental factor. When accessibility, mobility, and urban functionality fail to track population growth, the strain falls not only on traffic, but on the durability of the entire market.

Why Tampa Bay Is the Better Answer

Tampa Bay, St. Petersburg, and Pinellas County tell a different story than Miami — and one that is substantially better supported by the underlying data.

Affordability Creates Stronger Return Foundations

One central distinction lies in affordability. Average monthly rents in Tampa stand at approximately $1,877, compared with roughly $2,704 in Miami — alongside meaningfully lower entry prices on the acquisition side. That gap is precisely what generates structurally stronger cash-on-cash returns in Tampa Bay.

A second, often underappreciated factor: the typical mortgage payment in Tampa is projected to fall below 30% of median household income in 2026 for the first time since 2022. That is more than a statistical footnote. It is a meaningful signal that demand can re-anchor across a broader and more durable base.

Population Growth Driven by Real Demand

The demographic picture is equally clear. Since 2020, more than 270,000 people have relocated to the Tampa Bay metro area — drawn primarily from the Northeast and Midwest, particularly New York, New Jersey, and Chicago.

For investors, this type of in-migration matters. It is not primarily speculative capital moving around the map. These are people resettling in the region to work, live, and raise families. That is precisely the kind of demand on which stable rental markets are built over the long term.

Less New Supply, More Stable Market Mechanics

Supply dynamics add further support. New multifamily construction in Tampa Bay is projected to decline to roughly 3,500 units in 2026 — down sharply from a record high of 12,500 units in 2024. For investors, this is a consequential shift.

When new supply contracts while demand holds steady, market mechanics improve noticeably. Competitive pressure eases, absorption becomes healthier, and rent growth no longer has to fight against a wave of new deliveries. That is precisely the configuration investors have been waiting for.

Infrastructure That Keeps Pace With Growth

A further distinction from more speculative markets lies in the depth of infrastructure investment. Hillsborough County and Pinellas County are not investing reactively — they are investing with a clearly defined long-term growth horizon. The region’s flagship project is the complete reconstruction of the Howard Frankland Bridge.

At approximately $865 million, it is the largest infrastructure undertaking in Tampa Bay history. The bridge connects Pinellas and Hillsborough counties, carries more than 200,000 vehicles daily, and is scheduled to open with new express lanes in spring 2026.

Running in parallel is the expansion of I-275 in Pinellas County. The I-275 Widening Project adds two new express lanes, is projected to reduce travel delays by up to 85%, and is expected to generate more than $1.4 billion in regional economic value — and to deliver those benefits 15 years ahead of the original schedule.

That depth of investment is the decisive differentiator. Tampa Bay is not just growing — the region is building the infrastructure to support that growth concurrently. For real estate investors, this is not a footnote. It is a structural advantage that translates directly into location quality, demand strength, and long-term market stability.

What Miami Has That Tampa Bay Doesn’t Need

Miami has international brand recognition. Miami has luxury demand. Miami has a compelling story. But Miami also has an investor base that has partially decoupled prices from local fundamentals. Buying in Miami today means competing not only against yield-driven capital, but against capital pursuing other objectives entirely — wealth preservation, lifestyle preference, or geographic diversification. For buyers with those priorities, current cash flow is often not the primary criterion. For us, it is.

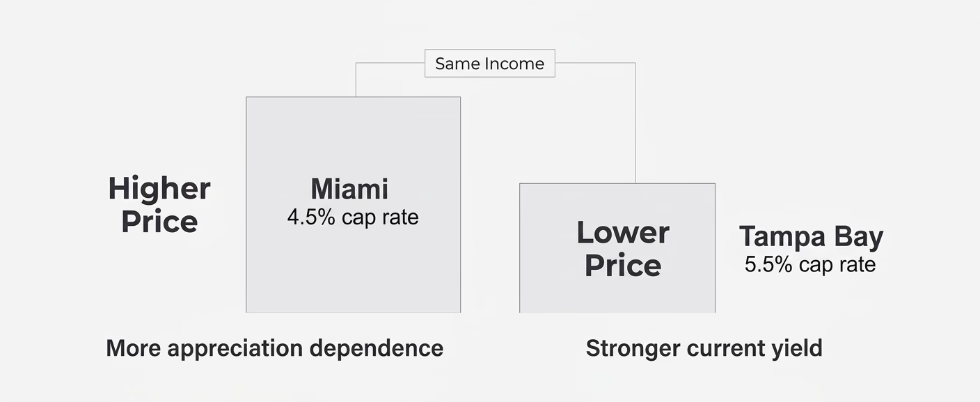

That dynamic is most visible in cap rates — and this is where the distinction becomes concrete for investors. Miami multifamily assets are currently trading at cap rates roughly 100 basis points below comparable assets in Tampa Bay. That may sound technical. In practice, it is a fundamental statement about investment quality.

A cap rate of 4.5% in Miami versus 5.5% in Tampa Bay means the investor in Miami is paying a substantially higher price for the same income stream. Operating income carries a smaller share of total return. The investment becomes correspondingly more dependent on future appreciation to generate acceptable performance. That is where the nature of the investment changes.

That is not an investment strategy. That is a bet.

A bet that becomes particularly demanding in a market carrying 19 months of supply overhang, declining prices, 32,000 units under construction, and strained infrastructure. Tampa Bay, by contrast, offers operating returns generated from ongoing income — financeable, plannable, and substantially less dependent on market euphoria. That is the difference between an investment grounded in fundamentals and a market that relies increasingly on future valuation assumptions.

Our Decision: Strategic Discipline Over Headlines

We invest in Tampa Bay because the market offers precisely what return-oriented investors require: defensible cash flows, demand-supported rent trends, and a demographic foundation that does not depend primarily on external capital flows. That is what distinguishes Tampa Bay from markets that function largely on the basis of visibility, brand, and international attention. The question for us is not which market has the best story. It is which market offers the more reliable investment logic over time.

Strong Fundamentals Do Not Replace Risk Discipline

As compelling as Tampa Bay’s fundamentals are: investors in Florida must account carefully for insurance and climate risk. Rising premiums, the divergence between coastal and inland submarkets, construction quality, flood zone exposure, and the real-world insurability of specific assets are not peripheral concerns — they are core components of the underwriting process.

For that reason, the question for us is not whether risks exist in Florida, but how they are managed. We are not investing indiscriminately in a high-growth state. We are investing selectively in locations and assets where demand, construction quality, insurability, and return profile stand in a defensible relationship.

Glamour sells well in content. Fundamentals pay the return. And when the market with the greatest media visibility simultaneously carries 19 months of supply overhang, falling prices, and the most intensive apartment construction activity in the entire United States, questioning the headlines is not a provocation — it is analytical discipline.

What This Means for International Investors

For investors based in Germany or the broader German-speaking world looking to enter the U.S. market, the essential question is straightforward: Am I buying a narrative, an image, a brand — or am I buying cash flow?

That is where market story and investment quality diverge. New York is excluded on regulatory grounds. So is Los Angeles. Miami, despite its appeal, no longer offers a price level, supply dynamic, and operating return that align with our approach.

Tampa Bay is neither the most glamorous market in Florida nor an undiscovered secret. But that is not the point. What matters is that in 2026, the market delivers what international investors need from a durable U.S. investment: stable demand, viable rental markets, reasonable entry prices, improving infrastructure, and returns generated from operations.

Not from hope. Not from hype. From fundamentals. That is why we are here.

Whitestone Capital focuses on U.S. multifamily investments in the Tampa Bay Corridor — for German and European investors seeking structured access to the U.S. market: tax-efficient, return-oriented, and without operational burden.