When a Pension Fund Starts Thinking Like a Real Estate Developer

Yield is tempting. Risk is exhilarating. “No pain, no gain,” or “no risk, no fun” — while these mantras may serve startups, hedge funds, and crypto forums, they have no place in retirement planning. The fact that these punchy slogans became a reality for a mandatory pension fund is not a theoretical exercise; it is the current reality at the Pension Fund of the Berlin Dental Chamber (VZB).

Studies show that many physicians delegate financial decisions to advisors. It is precisely for this reason that one should expect a pension fund to maintain an especially conservative, low-risk, and structurally robust investment portfolio.

Reports suggest the fund invested in a manner more reminiscent of a speculative developer than a retirement institution. Thousands of members now face potential pension cuts or significant financial losses.

What Happened? (Status: Winter 2026)

The pension fund, which manages contributions from approximately 11,000 dentists across Berlin, Brandenburg, and Bremen, is facing an existential financial crisis due to high-risk investment strategies.

- According to internal data and media reports, roughly €1.1 billion could be affected — approximately half of the total assets under management of €2.2 billion.

- Losses stem from high-stakes investments: startups, corporate project stakes, luxury hotels, and specialized real estate, as well as insufficiently collateralized loans that turned into failed investments.

- Experts and internal critics question whether these assets were ever compatible with the fiduciary duty of a pension fund — some even point to violations of internal guidelines and regulatory requirements.

This is not an academic debate. It is a practical reality: in Berlin, the traditional protective function of a pension fund was replaced by a speculative strategy that would be considered entirely inappropriate and reckless for traditional insurers or pension funds.

The Core Dilemma

Pension funds are neither hedge funds nor private equity playgrounds. Their mandate is clear: the long-term safeguarding of retirement benefits, not short-term profit maximization.

Yet at the VZB, these boundaries were blurred — and the consequences are now being felt by current and future retirees alike.

In fact, some dentists find themselves in such a precarious position that they are calling for political intervention and state bailouts to prevent total loss.

Luxury Resorts, Startups, and Development Projects – No Portfolio for a Pension Fund

A significant portion of the fund’s capital did not flow into traditional residential or office holdings with stable lease agreements, but rather into highly cyclical, capital-intensive structures.

According to media reports, this included:

- Substantial stakes in startups

- Luxury resorts in Ibiza and Sardinia

- Large-scale project developments

- Operating real estate

- Complexly structured special projects

Such investments can yield high returns – in a success scenario.

However, they are not predictable cash-flow instruments. They depend on market cycles, financing costs, exit windows, and management quality.

Startups statistically factor in high failure rates. Resorts depend on tourism flows and economic sentiment. Project developments are hostage to construction costs, interest rates, and marketability. Operating real estate stands or falls with individual tenants or management structures.

These are entrepreneurial risks, not actuarial ones.

The interest rate pivot of 2022/23 exposed the vulnerability of such constructions: rising financing costs, declining valuations, and closed exit markets. Models built on optimistic assumptions buckled under the pressure.

Reports indicate that engagements totaling up to €1.1 billion were affected — more than half of all funds. A share that is no longer a mere allocation, but a strategic concentration.

And this is where the actual problem begins:

A pension fund is allowed to take risks. But it must not change its mandate.

Retirement provision means predictable obligations, long-term stability, and high risk-bearing discipline. Anyone who systematically enters illiquide, highly volatile, and exit-dependent projects abandons the conservative core of institutional provision.

This is not a question of individual failures. It is a question of portfolio philosophy.

Return Targets and Realities

Double-digit IRRs do not originate from stably leased apartment buildings.

They are generated through:

- Leverage

- Project development gains

- Increasing exit multiples

- Optimistic market assumptions

Anyone calculating a 12 or 15 percent internal rate of return is implicitly planning for value appreciation, sales proceeds, and favorable financing. This is no accident; it is a model assumption.

As long as markets rise, this model works.

However, when interest rates and valuations pivot – as they did in 2022/23 – the logic flips. Financing becomes more expensive. Exit windows close. Valuations drop.

That is when it becomes clear whether a strategy was based on stable cash flows — or on scenarios.

And here lies the crux: If a pension fund systematically pursues return targets that are only achievable with entrepreneurial risk, it shifts its profile from provision to speculation.

This is not a single error. This is a strategic choice.

Why Does a Pension Fund Massively Shift Its Risk Profile?

It is a valid question. The answer is more complex than simple “greed.”

1. The Low-Interest Rate Dilemma

For years, zero and negative interest rates prevailed. Classical assets such as:

- Government bonds

- Mortgage bonds (Pfandbriefe)

- Core real estate

yielded barely enough to suffice.

Pension funds were under pressure to earn the guaranteed technical interest rates. Conservative portfolios were mathematically no longer sufficient.

The temptation to seek “a little more yield” became structurally greater.

2. Comparative Pressure

Institutional investors compare themselves to one another.

When private equity funds report 15% IRRs and project developers achieve double-digit returns, a psychological effect takes hold:

“Why should we settle for 3–4%?”

But this comparison is systemically flawed. A pension fund is not a yield competitor.

3. The Illusion of Predictability

Project developments and startups rarely present themselves as “speculation.” They arrive as business plans.

- With sensitivity analyses

- With cash-flow projections

- With exit scenarios

- In Excel, they appear controllable. In reality, they are cyclical.

The longer the boom lasts, the more stable the model appears. Until the cycle turns.

4. Governance Shift

When decision-making bodies increasingly adopt an entrepreneurial mindset, the understanding of risk shifts imperceptibly. Not abruptly, but step by step.

A “mix” becomes a “strategic allocation.” An “opportunistic investment” becomes a “yield driver.” Eventually, the portfolio is structurally aligned with something other than its mandate.

Startups – Structurally Alien to a Pension Fund

Venture capital investments operate according to a distinct logic:

- High failure rate

- A few extreme winners

- Long capital lock-up periods

- Illiquidity

- Valuation based on future expectations

In professional VC portfolios, total losses are not the exception; they are statistically factored in. The model relies on individual “unicorns” overcompensating for many failures.

For a venture capital fund, this is normal. For a pension fund, it is systemically alien.

Because a retirement provision requires:

- Predictable cash flows

- Reliable valuation

- Calculable risks

- High liquidity discipline

Startups provide none of the above.

If such holdings are not managed as a strictly limited peripheral allocation, but rather in significant volume, the risk profile of the entire portfolio shifts.

And that is the core of the criticism: Not that individual startups fail, but that they structurally do not fit the risk logic of a pension institution.

The Fundamental Error

Yield cannot be viewed in isolation. Anyone playing the right side of the risk/return matrix automatically receives the accompanying volatility.

One cannot:

- Seek opportunistic returns

- Take on project development risks

- Accept cyclicity

- and simultaneously guarantee stability

This is economically contradictory. The fundamental structure of a pension fund should consist of long-term, solid cash-flow generating assets (e.g., residential real estate, bonds, dividend stocks) with allocations in higher-yield investments such as startups or riskier real estate holdings.

The alternative to startups and resorts would not have been a surrender of yield. It would have been a different choice of risk.

Balancing Yield – Without Startups and Resorts

In our consulting for family offices and institutional investors, we see the same pattern time and again:

Yield is not an either-or proposition. It is a question of structure.

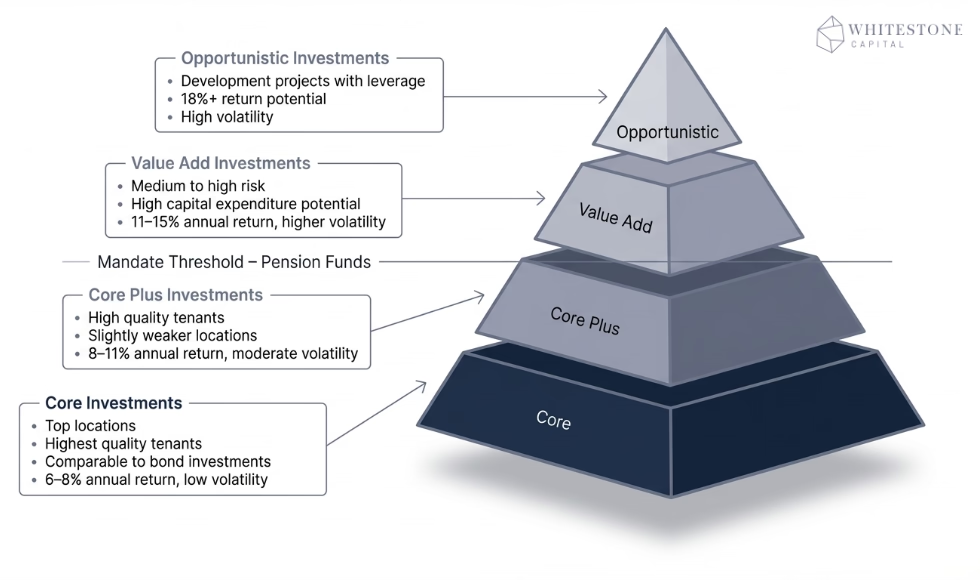

In professional real estate investment, one systematically distinguishes between four strategies:

- Core: Stabilized properties in prime locations, fully leased, low fluctuation, predictable cash flows.

- Core Plus: Solid assets with slight optimization potential, moderate risk, slightly higher yield.

- Value Add: Repositioning, modernization, vacancy reduction – higher management intensity, higher cyclicity.

- Opportunistic: Project developments, resorts, specialized real estate, high leverage, exit dependency – with corresponding risk.

The further one moves up this matrix, the more sharply these factors rise:

- Construction cost risks

- Financing risks

- Valuation volatility

- Exit risks

A pension fund is not restricted in this choice. It can invest conservatively or entrepreneurially. This is precisely what makes the strategic decision so central.

Yield can also be achieved in the lower and middle sections of the matrix – just not spectacularly, but structurally.

A portfolio of Core and Core Plus properties, supplemented by limited Value Add portions, can generate stable returns without being existentially dependent on exit windows or market cycles.

The question, therefore, is not “Why real estate?” but “Why this risk class?”

Responsible Yield is Neither Luck Nor Coincidence

Yield does not arise from courage alone, and certainly not from the hope for the right exit. It arises from structure, discipline, and a clear definition of the mandate.

Those who manage long-term obligations do not need a spectacular yield promise; they need a resilient risk concept. Proper allocation decides the outcome – not the highest target yield in a model.

In supporting family offices and institutional investors, we see it repeatedly: Stability is not a product of chance. It is the result of deliberate weighting. Core as the foundation. Selective opportunities as a minor allocation. Clear boundaries for entrepreneurial risk.

Yield can be balanced. But only if it serves the mandate – and not the other way around.