Donald Trump has brought the issue back onto the agenda. With his announcement to exclude institutional investors from purchasing single-family homes, he delivered a political bombshell that immediately caught on. In public debate, this quickly became the buzzword of the “Wall Street ban” – simple, catchy, and emotionally charged.

The underlying assumption is clear: Large financial players are buying up the US single-family home market, depriving private buyers of housing. But this is where the problem starts. This narrative only partially holds up under a sober analysis of market data.

Who exactly should be affected? How significant is the actual influence of institutional investors on the US single-family home market? And what real impact would such a ban have – beyond political symbolism?

For investors, this debate is more than election rhetoric. It shows how quickly complex market mechanisms are reduced to simple blame games – and why solid market knowledge is crucial in regulation-sensitive times.

“People Live in Houses, Not Corporations” – Why the Myth of Investor Buying Doesn’t Hold Up

“People live in houses, not corporations.”

The phrase is catchy, morally charged, and politically highly effective. It suggests that institutional investors are systematically buying up single-family homes, removing them from the ownership market, and thereby taking housing away from private buyers.

This assumption forms the emotional foundation of the current debate. The problem: It only partially withstands a data-based analysis.

Since 2016, there hasn’t been a massive influx of purchases by investors – quite the opposite. Net, around 1.5 million single-family homes have disappeared from the rental segment in the US because private owner-occupiers have outpaced investors in competing for existing properties. This conclusion comes from sources like John Burns Research and the Harvard Joint Center for Housing Studies.

In other words: It’s not investors displacing owner-occupiers, but owner-occupiers pushing investors out of the market.

Executive Order Instead of Law – What Trump Actually Decided

Key is first a clean classification: So far, there is no law prohibiting institutional investors from buying single-family homes. Trump’s initiative is at the level of an Executive Order – a political signal, not an immediately effective regulation.

Such an order does not create a purchase ban on its own. It rather marks a political direction and theoretically opens the way to later legislative or regulatory measures. The gap between announcement and actual intervention is large – and legally anything but straightforward.

Indeed, the Director of the Federal Housing Finance Agency (FHFA), Bill Pulte, told CNBC that the White House has “a whole range of tools” to implement such a plan. But which tools those are specifically remains open. This is the core of the uncertainty.

Neither reliable draft laws exist, nor is it foreseeable how such a regulation would need to be legally structured to withstand judicial review. For investors, this means: lots of political rhetoric, but so far little operational substance.

Who Exactly Should Be Excluded? – A Ban Between Ineffectiveness and Collateral Damage

The crucial question is not whether a ban is politically desired, but who it should specifically target. And this is the core of the problem: To date, there is no reliable definition.

Trump himself speaks of “institutional investors.” In the real estate industry, this usually means a very small group of large players – often investors with portfolios of 1,000 or more single-family homes. Such a demarcation would be narrow, clear, and legally manageable.

Precisely because of this, it would largely devalue the initiative.

A ban that affects only a handful of market participants would have hardly measurable impacts on supply, prices, or affordability. Politically, it would be loud, but economically almost ineffective. The narrower the definition, the greater the likelihood that the ban effectively falls flat.

For this reason, increasingly vague terms like “corporations” or “corporations” appear in political communication. This wording opens up room for maneuver – but carries significant risks. Consistently thought through, such definitions would also capture smaller private investors who invest through LLCs for liability or structuring reasons. Precisely those “mom-and-pop” owners who politically shouldn’t be meant.

This creates an irresolvable tension: A narrow definition is politically ineffective. A broad definition is economically and legally problematic.

Regardless, one central fact remains: Around 90% of the single-family rental market is still carried by small private investors. A ban that ignores this market structure either misses its target – or hits the wrong players.

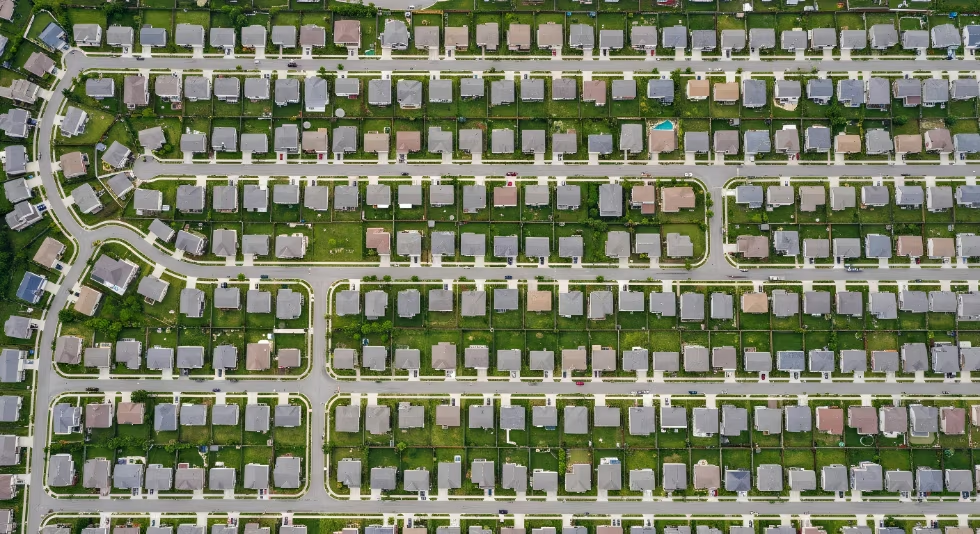

How Many Single-Family Homes Are Really Affected? – Three Numbers, a Distorted Picture

Few aspects of the debate are as misleading as the question of the actual scope of institutional investors in the US single-family home market.

The reason: In public discussion, three completely different metrics are regularly mixed – deliberately or unconsciously.

First, it is often pointed out that institutional investors hold around 2–3% of the single-family rental market (SFR). This number sounds relevant but describes exclusively the rental market. It says nothing about how large the influence of these players is on the entire stock of single-family homes.

Second, the actual share of institutional investors in the entire single-family home market is only around 0.7%. Specifically, institutions own about 600,000 homes out of a total of around 87 million single-family homes in the US. Even this number loses drama once contextualized: It corresponds to less than the volume of new single-family homes built in a single year. Mathematically, the market can thus compensate for this “problem” within twelve months.

Third – and particularly inconvenient for the political narrative – the share of institutional buyers in actual home sales in recent years was just around 0.5% of all transactions. Anyone wanting to explain rising prices or lack of affordability must therefore look at other causes.

In short: Institutional investors are omnipresent in public debate. In the market itself, they are numerically small.

What Would Be the Actual Impact of a Ban?

Based on everything known so far, institutional investors should not be forced to sell existing holdings. Trump’s initiative aims solely at preventing future purchases of single-family homes. It’s not about dismantling inventories, but limiting future transactions.

Even in this scenario, the impact remains manageable. Institutional buyers currently account for only around 0.5% of all home purchases. A complete exclusion would thus change the market only at the statistical decimal point – with barely measurable effects on prices or affordability.

Realistically, the influence turns out even smaller. Because these 0.5% refer solely to gross purchases. What matters for market impact are net flows – purchases minus sales. And here, a picture emerges that contradicts the political narrative: Institutional landlords have recently been more often net sellers than net buyers.

Even more significant is a point almost completely overlooked in the debate: The market has structurally evolved long ago – politics is discussing an outdated picture. Large institutional investors today rarely buy individual single-family homes in open competition. Instead, they acquire entire single-family rental portfolios or cooperate directly with developers.

The largest SFR owner in the US, Pretium (Progress Residential), has communicated this openly. The company does not buy via the MLS, i.e., not through the classic marketplace where private owner-occupiers and investors compete for the same homes. These transactions occur outside open competition and do not deprive private buyers of properties.

In other words: A buying behavior is being regulated that hardly exists in this form anymore. The political focus is on a market segment that is no longer the dominant mechanism.

Even if all that is ignored, another inconvenient truth remains: It is extremely unlikely that the homes bought by institutions would otherwise automatically go to owner-occupiers. Especially for renovation-needy or undervalued properties that institutional buyers typically prefer, smaller investors could easily fill this demand.

In summary, one clear insight remains: This ban will primarily produce headlines. It will hardly bring measurable benefits for people wanting to buy a home.

BlackRock and the Question of Single-Family Homes

In public debate, one name appears particularly frequently: BlackRock. It stands symbolically for “Wall Street,” for financial power, and for large capital flows. That’s why BlackRock is often linked to the accusation that institutional investors are systematically buying up single-family homes from American families.

However, this notion falls short – mainly because it fundamentally misunderstands BlackRock’s role.

BlackRock is primarily an asset manager. The company manages capital on behalf of third parties: pension funds, insurers, foundations, states, and millions of private investors. BlackRock does not decide freely over its own capital but implements investment decisions within clearly defined mandates. The company is not an operational real estate buyer that purchases, manages, and rents homes itself. Accordingly, BlackRock holds no own single-family homes and does not appear in the single-family home market as a direct owner.

What is usually meant in public discussion is Blackstone – a completely different company, a similar name, a different business model. Blackstone is a so-called alternative asset manager. The company raises capital in funds and invests it actively in real assets: companies, real estate, infrastructure, credit portfolios. Blackstone is thus actually operationally active in the real estate market – including in the residential segment.

Yet even with Blackstone, a closer look is worthwhile. The assumption that large platforms would permanently and aggressively accumulate single-family homes only partially withstands reality. Blackstone has repeatedly pointed out that in recent years, it has been more of a net seller of residential properties. The stock of single-family homes has not been expanded but reduced.

The reason for this is not political, but commercial.

Single-family homes are a structurally challenging asset for very large, centralized capital. They consist of thousands of individual properties with unique building substance, location, maintenance needs, and tenant structures. Unlike large apartment complexes, processes can only be standardized to a limited extent. Management, maintenance, and leasing cause high operational costs relative to the invested capital.

Added to this is the question of capital commitment. Institutional investors constantly compare: multifamily, logistics, data centers, infrastructure, credit strategies. Single-family homes provide stable cash flows but often do not achieve the risk-adjusted returns that large funds can realize compared to other asset classes. The exit logic is also complex: Individual sales are time-intensive, package sales depend heavily on market phases and buyer circles.

Another factor is the regulatory and political environment. This very debate shows how quickly single-family homes can become a political symbol. For large platforms, this means reputation and regulatory sensitivity – a risk increasingly considered in investment decisions.

All this expressly does not mean that single-family homes are bad investments. For private or semi-professional investors with local know-how, long-term horizons, and manageable structures, they can be very attractive. The key distinction is different: What makes sense for private capital does not necessarily work for institutional large capital.

Anyone ignoring this differentiation mixes business models, incentive systems, and realities – and thus misses the core of the debate.

Affordability Remains the Core Problem

The crucial question for buyers is not who buys homes, but who can afford them at all. This is where a possible purchase ban for institutional investors misses its starting point.

Even if these players completely disappeared from the market, it would have no measurable effect for most renters. The central hurdles on the path to ownership remain – regardless of whether institutional investors buy or not.

According to calculations by John Burns Research and Consulting, buying a typical entry-level single-family home in the US currently costs over $1,000 per month more than renting a comparable property. This gap is the result of purchase prices, interest rates, and credit conditions – and it doesn’t disappear through regulatory interventions on the buyer side.

Added to this is a structural financing problem. A significant portion of households already fails at the entry requirements for a mortgage. Stephen Scherr, Co-President of Pretium (one of the largest operators of rented single-family homes in the US), put it unmistakably on CNBC:

“More than half of the adult US population would not get a mortgage loan today.”

The typical renter household at Pretium earns an annual income of around $130,000 – yet about 90% of these households do not receive real estate credit.

The problem is thus not primarily lacking income, but the combination of credit standards, equity requirements, and risk assessment.

And even households that would basically be creditworthy often hit the next barrier: the down payment. Equity remains the biggest entry hurdle into the ownership market for many potential buyers – completely independent of whether institutional investors are active or not.

Against this backdrop, it becomes clear why a purchase ban can hardly have an effect. It does not address the causes of lacking affordability but shifts the focus. Or put differently: The core problem lies in financing, equity, and credit access – not in a buyer segment that makes up only a fraction of the market.

New Constructions, Regulation, and Financing – Why Political Signals Still Hit the Market

To understand why the discussion about a purchase ban for institutional investors is unsettling the market, even though their actual market share is small, one must look deeper. What matters less is who buys, but how new construction is financed and secured.

At the center is the Federal Housing Finance Agency (FHFA). It is the supervisory authority over Fannie Mae and Freddie Mac – two institutions through which a significant part of US housing financing runs. Anyone changing the rules here does not intervene directly in purchase decisions but in the financing foundation of the entire market.

The current FHFA Director Bill Pulte has positioned himself clearly on this issue. His statement that new homes should “go to people, not corporations” is less a technical assertion than a political signal. Pulte clearly stands on the side of ownership-oriented housing policy – and uses the lever his agency offers: the conditions under which mortgages are financed, guaranteed, or excluded.

Why is this relevant for new constructions?

A significant portion of new single-family homes today is not built exclusively for classic owner-occupiers. Developers often secure sales and financing through pre-sales to professional operators of rented single-family homes, so-called SFR platforms (Single-Family-Rental platforms). These platforms do not buy individual homes in the open market but entire tranches or projects directly from the developer.

For developers, this has tangible advantages:

- Planning security: A portion of production is already sold.

- Risk reduction: Less dependence on end-customer financing and interest cycles.

- Financability: Banks positively evaluate secured buyers.

Important here: These sales occur outside the classic buyer market. Private owner-occupiers do not compete here with institutional buyers for the same property.

This is exactly where political criticism sets in. Pulte argues that institutional buyers sometimes receive better terms from developers. Economically, this is not a privilege but a consequence of volume, speed, and payment security. Politically, however, it acts like favoritism – and is addressed accordingly.

The problem: If this sales and financing channel is restricted, not only demand changes, but supply. Higher risks and worse financing conditions lead to projects being realized later, smaller, or not at all. Particularly affected are build-to-rent structures, which represent a relevant part of new construction volume in many regions.

This makes it clear why this debate has an impact despite low market shares of institutional buyers. It intervenes not at the margin but at the foundation of new construction financing. The mere announcement of possible interventions is enough to make investors, banks, and developers more cautious – long before a formal ban exists.

The political message is to protect homeownership. The economic consequence could be that less housing is created. Precisely this tension makes the discussion relevant for investors – not as a headline, but as a signal.

Build-to-Rent Communities – A Different Segment with Different Logic

In the discussion about a possible purchase ban, the question inevitably arises of how classic build-to-rent communities (BTR) are to be classified. These are new construction neighborhoods of single-family homes or townhomes specifically developed for the rental market.

Structurally, these facilities resemble apartment complexes more than the classic single-home market. The units are on contiguous lots, centrally managed, and legally not intended for individual sale. A later division into individual ownership units would only be possible through a complete conversion to a condo structure.

Precisely for this reason, it is unlikely that a purchase ban for single-family homes could be directly applied to BTR communities. They do not compete with owner-occupiers for existing properties but expand the rental supply in the new construction segment.

Theoretically, there is an indirect regulatory lever through financing. Through its supervisory function, the Federal Housing Finance Agency could influence Fannie Mae and Freddie Mac and exclude certain BTR structures from financing. Such a measure would significantly impair the liquidity and feasibility of these projects.

Crucial, however: Such a step is considered extremely unlikely even under current political signs. For that, BTR is too closely linked to classic multifamily logic – and too relevant for the new construction volume of many markets. An intervention would hit less investors than reduce the overall housing supply.

Are Forced Sales Conceivable?

One of the most common concerns in the current debate is whether institutional owners could be forced to sell their already held single-family homes. Based on what is currently known, there are no reliable indications for this.

While there have been political initiatives in the past that aimed to force a de facto inventory reduction through tax penalties. Trump has expressly distanced himself from this approach. His statements do not aim to dissolve existing portfolios but to limit future purchases of single-family homes.

This distinction is central. A forced sale of existing holdings would deeply intervene in property rights, entail significant legal risks, and trigger massive market disruptions. Precisely for this reason, there is currently neither the political will nor a viable legal basis for it.

Interesting in this context is the position of the National Association of Realtors (NAR). The organization calls on political decision-makers to create incentives for investors to sell homes. Officially, this is justified with the goal of higher affordability.

Economically, however, the effect is clear: More sales mean more transactions – and more transactions mean more commissions. For broker organizations, it’s obviously not about an abstract housing policy objective but about a business model that lives off as high turnover as possible. Every additional sale generates brokerage fees, regardless of whether structural affordability improves or not.

This doesn’t automatically make the demand illegitimate but puts it in the right context. Also in this debate, interests are at play – and they don’t always align with the public narrative of “more supply for buyers”.

In summary: A politically forced mandatory sale of institutional SFR holdings is not foreseeable at present. The actual direction of the discussion clearly lies on future purchases. Demands for inventory reduction stem less from regulatory reality than from economic self-interests of individual market players.

How Do Economists and Market Participants React? – Criticism Beyond the Investor Question

The political initiative may convince emotionally, but in the expert world, it meets with clear opposition. Notable is less a single counterposition than the breadth of criticism. Housing economists and real estate analysts from different political camps independently arrive at similar assessments.

The Washington Post summed up this consensus:

“Many economists – both from the right and the left – say that investors do not have the housing market in their grip nearly as much as politicians sometimes portray.”

The objection is not against regulation per se, but against the diagnosis. Anyone naming institutional investors as the main cause of rising prices, according to many experts, falls short – and overlooks structural factors.

Opposition also comes from the industry itself, albeit notably factual. Large providers in the single-family rental segment avoid polemical counterattacks and instead refer to market mechanics. This applies especially to platforms that – as already described – have withdrawn from aggressive individual purchases of existing homes for years and increasingly focus on new construction and build-to-rent structures.

Some market participants have nonetheless taken a clear stance. Sean Dobson, CEO of Amherst, put it unmistakably on Bloomberg TV:

“Preventing investors from investing capital in the housing market will not improve affordability.”

Dobson thus points to a point shared by many critics of the initiative: Displacing capital from the housing market does not solve a supply bottleneck. At most, it shifts it.

Another aspect that relativizes the political narrative concerns the actual buying behavior of large players. Several providers emphasize not acting in open competition with owner-occupiers. Instead of individual existing properties, portfolios are acquired or directly cooperated with developers – often to secure new projects, where the majority of units still go to private buyers.

Even the symbolic figures of the debate mentioned earlier fit only partially into the simplified picture. Blackstone publicly declared having been a net seller of residential properties in the past ten years; its own stock has decreased by more than 20%. BlackRock, often mentioned in the same breath, is – as explained before – primarily an asset manager and not an operational buyer of single-family homes.

Also the National Rental Home Council, the industry association of professional SFR providers, points to the dimensions:

“Professional providers of single-family homes for rent make up only a small part of the overall housing market.”

In a later statement, it was formulated even more fundamentally:

“Restricting investor participation does not solve the fundamental problem of lacking affordability. The high costs of homeownership are the result of limited supply – and excluding investors does not increase this supply.”

In summary, a clear picture emerges: The political impulse is easy to convey. The expert assessment turns out much more critical. Anyone wanting to explain the affordability crisis must talk about supply, new construction, and financing – not just about investors.

Conclusion – A Popular Impulse, But No Market-Effective Solution

The political initiative to exclude institutional investors from buying single-family homes lives off its simplicity. It offers a clear enemy image, an easily understandable measure, and the promise of quick relief. That’s exactly what makes it politically attractive.

Economically, however, this logic does not hold.

Institutional investors are neither the dominant buyer nor the central price driver in the US single-family home market. Their actual market share is small, their buying behavior more differentiated than the public narrative suggests. Many of the players regularly named do not buy in open competition with owner-occupiers or have long scaled back their activities.

Above all, the ban does not address the real problem. The affordability crisis is not the result of individual buyer groups but the outcome of structural bottlenecks: too little new construction, high financing costs, strict credit standards, and lacking equity.

Where institutional capital plays a role today – in new constructions, pre-sales, and build-to-rent structures – it often stabilizes the supply side. If this mechanism is politically restricted, the risk increases that less is built.

In short: The political impulse may be popular. The economic logic behind it is not.