The recent municipal elections in North Rhine-Westphalia delivered an unmistakable signal. The substantial loss of voter support suffered by the SPD was driven neither by communication failures nor by personnel, but by an economic-policy stance that no longer holds up against the underlying realities of Germany as a business location. Yet rather than a substantive course correction, the response follows a familiar pattern: calls for sweeping redistribution programs, higher top-bracket tax rates, and the levying of so-called “excess profits” are growing louder. This is no political coincidence. It is the symptom of a fiscal-policy debate in Germany that increasingly operates in the moral domain – having long since departed the economic one.

“The Wealthy Don’t Pay Enough” – a Phrase That Feels Right but Explains Little

The demands are familiar: raise top tax rates, increase the burden on capital income, finally tax inheritances ‘properly,’ and skim off ‘excess profits.’ These are terms that work politically because they channel public outrage. Economically, they are considerably more difficult to operationalize.

Consider the construct of the “excess profit.” In political parlance, it refers to a profit that is simply perceived as too high. In economic theory, the term does not exist.

Markets do not produce “normal” returns on demand. They produce returns as a premium for assumed risk, intelligent capital allocation, market demand, and precise timing. A tax levied on economic outcomes that are retrospectively judged “too good” is, in effect, a penalty on successful investment decisions. The consequence is foreseeable: it dampens the willingness to commit to the next investment. Who defines what is “fair,” and where is the line drawn? These questions are consistently absent from the current debate – because the mathematical answers would be inconvenient.

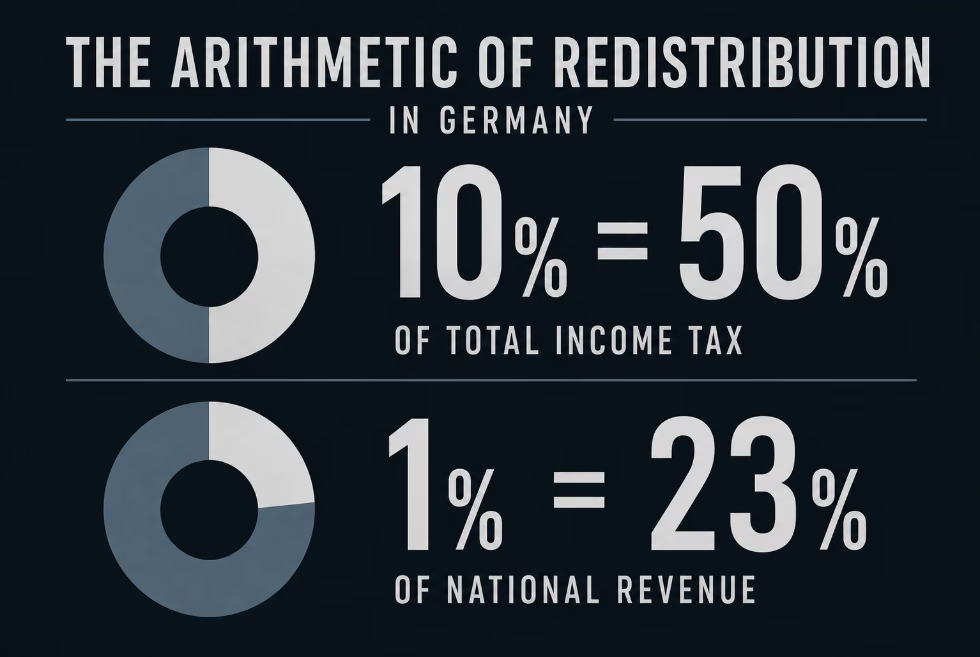

The Arithmetic of Redistribution: Who Actually Pays?

Germany operates one of the most progressive tax systems within the OECD. This is not a political assertion but measurable reality.

A look at the data published by the German Federal Ministry of Finance reveals the actual distribution of the burden: the top 10 percent of income earners contribute more than 50 percent of total income tax revenue.

The top 1 percent – which earns roughly 12 percent of total income – alone funds approximately 23 percent of the national tax base. The mathematical conclusion is unambiguous: redistribution in Germany is already in place. On a substantial scale, structurally, and permanently.

Anyone calling for further burdens on top earners against this backdrop must answer one central economic question: what, precisely, has the existing comprehensive redistribution achieved – and why should an intensification of the same mechanism suddenly produce better macroeconomic outcomes? The current debate has yet to provide that causal explanation.

A Side-by-Side Comparison: The Tax Burden in the U.S. vs. Germany

An analytical comparison of the two tax systems (at the federal level) produces an unambiguous empirical picture: while the United States sets incentives for capital formation and investment, Germany focuses on early and far-reaching extraction.

Personal Income Tax

The U.S. top federal income tax rate stands at 37 percent and only applies to single filers from a taxable income of USD 626,350. In Germany, the top rate of 42 percent already kicks in at a taxable income of just EUR 66,761. German tax progression therefore withdraws the liquidity required for private capital formation considerably earlier in the income curve.

Capital Gains Tax & the German Vorabpauschale

In the United States, long-term capital gains are taxed at 0, 15, or 20 percent depending on overall income – supplemented by a Net Investment Income Tax (NIIT) of 3.8 percent for the highest income brackets. Germany, by contrast, applies a flat capital gains tax (Abgeltungsteuer) of 25 percent plus solidarity surcharge.

Germany’s true structural disadvantage, however, lies in its withdrawal of liquidity: through instruments such as the Vorabpauschale (advance lump-sum tax), the German tax authority levies a charge even on unrealized book gains within investment vehicles.

A mechanism that severely impedes the compounding effect – whereas the U.S. system (for instance, through depreciation allowances in real estate) deliberately favors tax deferral and reinvested, compounding growth.

Corporate Taxation

The U.S. federal corporate tax rate remains at an internationally competitive 21 percent. In Germany, the combined burden of corporate income tax and trade tax quickly amounts to roughly 30 to 32 percent. For anyone allocating capital strategically, this represents a clear mathematical arbitrage opportunity.

An important caveat: the geography of the tax burden

These figures primarily reflect the U.S. federal level. While some U.S. states do levy additional state taxes, this is precisely where the actual capital allocation strategy comes into play: in high-growth Sunbelt states such as Texas or Florida, the state-level income tax stands at zero percent. The tax burden, then, can not only be compared but actively minimized through geographic precision.

The Strategic Lever for DACH Investors: Tax Structure and the Preferred Return

What the German tax debate systematically overlooks: the favorable U.S. tax rates and market structures are not theoretical concepts. They are directly accessible to German and European investors through intelligent capital allocation – entirely legally, transparently, and by political design.

Investors from the DACH region who deploy capital into U.S. real estate through specialized vehicles benefit from three decisive structural levers:

Cash Flow Priority (Preferred Return)

Whereas many European fund models prioritize high management fees at the expense of initial returns, professional U.S. structures are dominated by the Preferred Return. The investor mandatorily receives the first cash flow distributions (typically 6 to 8 percent per annum) before the sponsor participates in profits at all. A systemic advantage that enforces an uncompromising alignment of interests.

The Tax Shield (Depreciation & Tax Treaty)

Thanks to the specific depreciation provisions in U.S. tax law, ongoing investment income from real estate remains effectively tax-free for many years. Tax becomes due only upon a later sale (exit), at a maximum federal rate of 23.8 percent. Under the clear provisions of the double taxation treaty (DTT) between the United States and Germany, this income is exempt from taxation at home and is subject only to the progression clause (Progressionsvorbehalt).

The Generational Strategy (1031 Exchange & Step-Up)

We opened this analysis with the current political push for tougher inheritance taxes in Germany. The U.S. system provides the maximum strategic counterpoint: instruments such as the “1031 Exchange” allow real estate sale proceeds to be rolled into new properties tax-free, in theory indefinitely (tax deferral). Combined with the “Step-Up in Basis” at intergenerational transfer, the tax-optimized buildup of family dynasty wealth in the U.S. is not a legal loophole but the deliberate design of the capital market.

The Logic of Capital Flight: A Behavioral-Economic Perspective

This fiscal-policy dynamic can be reduced to a simple but instructive behavioral-economic model:

When one guest at a table is already covering more than half of the entire bill for everyone present, and is then told that his contribution is morally insufficient and must necessarily be raised, the consequence is foreseeable.

He will not engage in a moral debate – he will simply choose a different venue for the next invitation. What would be recognized as toxic and illogical in everyday social life is being sold as “justice” in German tax policy.

The reality, however, remains the same: capital and high performers do not debate morality indefinitely. They leave the restaurant.

They redirect their resources to jurisdictions that value economic performance as necessary fuel rather than treating it as a permanent object of suspicion.

Conclusion: A Clash of Mindsets – Redistribution vs. Value Creation

The U.S. system is not a legal tax trick but the calculated outcome of a functioning international architecture that deliberately attracts investment.

Ultimately, the fundamental difference between the two jurisdictions lies not in the statutes but in the underlying economic DNA: the German debate increasingly treats private capital as an object of suspicion and the economy as a zero-sum game – and from that perspective, entrepreneurial success must necessarily be siphoned off in order to generate moral justice.

The U.S. system, by contrast, treats capital as necessary fuel. It does not penalize success ex post but incentivizes risk-taking ex ante. It rests on the deep conviction that an expanding value-creation base is the most effective form of safeguarding prosperity.

Raising the marginal tax burden above a certain threshold changes more than just the tax bill – it irrevocably changes investment decisions. Anyone vocally debating higher capital taxes in Germany should be aware of this global context: a substantial share of the capital that would otherwise remain within the German system can be redirected entirely legally into a system with a superior mindset and stronger incentive structures.

Anyone seeking to redistribute on a sustained basis must first understand where value is created – and what happens when the framework conditions for that creation begin to erode. For investors in the DACH region currently reviewing their capital allocation, this comparison of mindsets is more than academic: it is the foundation for concrete, legally executable action.

This is neither a right-wing nor a left-wing position. It is arithmetic.