Return Driver or Structural Refinancing Risk?

If you regularly review multifamily investment decks, you know the pattern:

- Refinancing in year 3.

- 70% of equity returned to investors.

- IRR increases significantly.

The model looks compelling. Investors receive capital back, remain in the deal, and benefit from what is often referred to as an “infinite return” or “cash-out refinance.”

On paper, this appears efficient. In practice, it is frequently a bet on capital market conditions.

The critical question is not whether a refinancing is feasible in principle. The critical question is whether it may be used as a load-bearing return assumption in the underwriting.

Once the projected IRR relies materially on a refinancing event, the investment profile shifts: from operational value creation toward interest rate, liquidity, and valuation risk.

This is not a minor modeling detail. It is a strategic risk transfer.

Based on our review of numerous business plans, we know: a refinancing is not an operational lever – it is an external variable. It depends on interest rates, cap rates, DSCR requirements, and credit availability at the time of refinancing.

None of these factors are within the investor’s control. And this is precisely where the real refinancing risk begins.

The Appeal of Refinancing

Let us be clear from the outset: refinancing is not inherently flawed. It is a legitimate tool in multifamily underwriting.

When a value-add business plan performs operationally – when net operating income (NOI) genuinely increases through renovations, rent adjustments, and cost optimization – property value rises accordingly, assuming a stable or favorable cap rate environment. In a stable debt market, a refinancing can then release capital without requiring an asset sale.

Investors receive equity back, remain invested, and continue to participate in cash flow. That is a strategically sound approach.

In an environment of falling or stable interest rates, this capital strategy can improve IRR, accelerate capital velocity, and reduce the equity contribution within the deal.

Up to this point, everything is sound.

The critical threshold is reached when refinancing is no longer modeled as an option – but as a prerequisite.

Once the projected return is only achievable if a specific loan amount at a specific interest rate can be secured in year 3 or 4, the investment’s risk profile has fundamentally shifted.

The return is no longer driven primarily by operational performance. It is driven by future capital market conditions. And those are neither stable nor controllable.

A refinancing depends on:

- interest rate levels at the time of refinancing

- lender appetite and credit availability

- debt yield and DSCR requirements

- property valuation based on prevailing cap rates

- overall liquidity conditions in the financial system

None of these variables are within the sponsor’s or investor’s control.

The issue is not the instrument itself. The issue is the dependency.

When a refinancing becomes necessary to justify the projected IRR, the underwriting has evolved from an operational analysis into an implicit macro bet. That is a fundamental distinction.

The Variables You Cannot Control

When you model rent growth, expense stabilization, or renovation premiums, you are assessing operational execution. You can analyze comparable properties. You can validate construction costs. You can speak with property managers. You can run sensitivity analyses.

These are operational risks. They are measurable. Partially manageable. Verifiable. Refinancing does not belong in this category.

It relocates the investment into an entirely different risk domain – the capital markets.

A refinancing depends on:

- interest rate levels in the refinancing year

- lender liquidity and credit appetite

- debt yield and DSCR requirements

- property valuation based on prevailing cap rates

- regulatory and macroeconomic conditions

If interest rates rise by 150 basis points, the supportable loan amount decreases significantly. If cap rates expand, valuations fall – even with on-plan NOI growth. If NOI falls short of projections, covenants may be breached.

None of these variables are within the sponsor’s control.

If the initial financing is fixed on a long-term basis, a failed refinancing typically means only a lower return.

However, if a bridge loan has been taken that must be refinanced within three years, structural pressure builds. The refinancing is no longer an option – it is a requirement. And that is precisely where the risk profile tips.

The Underestimated Incentive Problem

There is another dimension that many models fail to address: the shift in risk incentives.

When a cash-out refinancing is executed in year 3, the following occurs:

- Investors receive capital back

- The sponsor collects ongoing fees

- Depending on the structure, promote may be triggered

- Leverage frequently rises back toward maximum loan-to-value

Following an aggressive refinancing, the loan-to-value is often higher than originally planned. The safety margin narrows. Downside risk increases.

At the same time, the capital structure shifts: the sponsor may have less of their own capital at risk in the deal. A portion of the economic upside has already been realized.

The investor, however, remains fully invested – now with higher leverage and a reduced buffer.

This is not a moral judgment – it is capital mechanics.

The more heavily the IRR depends on an interim refinancing, the more important the question becomes: who carries the remaining risk after the refinancing – and with what equity contribution?

In boom phases, this appears efficient. In stress phases, it is precisely this structure that determines stability or capital loss.

The Structural Distinction: NOI Growth vs. Cap Rate Bet

Not all refinancings are equal. A refinancing grounded in real, sustainably improved NOI is qualitatively different from one that depends on cap rate compression or favorable debt availability.

In the first case, additional value is created through operational improvement. In the second, it derives from market conditions.

The distinction is fundamental: operational performance can be influenced. Cap rates and interest rates cannot.

When a refinancing is primarily driven by valuation assumptions, the underwriting embeds a macro forecast into the return structure. But macro forecasts are cyclical.

The Principle We Apply

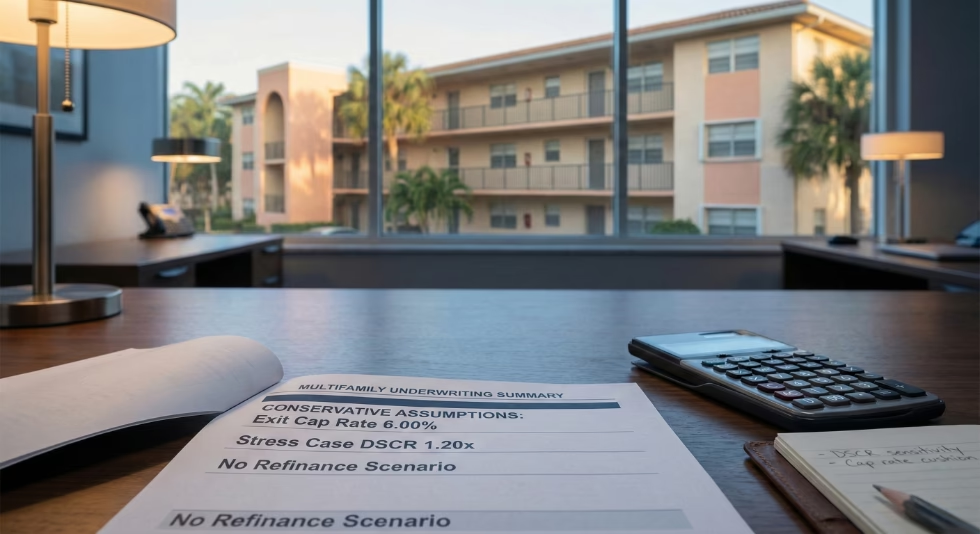

In our underwriting, we follow a clear and non-negotiable principle: The deal must work without a refinancing.

This means an investment must meet the defined risk threshold based solely on operational performance and a conservatively modeled exit scenario. Cash flow should be sustainably positive from acquisition – or at the latest upon completion of the value-add program. Debt service coverage (DSCR) must remain viable even under stress assumptions. Financing should be fixed on a sufficiently long-term basis to limit interest rate risk and avoid creating artificial refinancing pressure.

The valuation methodology is equally critical. The exit cap rate must account for potential expansion and must not implicitly assume further compression. Underwriting that relies on declining cap rates embeds a market forecast into the return structure. Sound underwriting, by contrast, is grounded in operational value creation and conservative capital structure – not valuation optimism.

The return must remain acceptable even if no interim refinancing takes place. The investment should be supported by stable cash flow, appropriate leverage, and realistic exit assumptions – not by the expectation of favorable capital market conditions in year 3 or 4.

If removing the refinancing from the model causes the projected IRR to collapse materially, the true structure of the deal is revealed. In that case, the refinancing is not an optional return enhancer – it is a load-bearing pillar of the calculation. And a load-bearing pillar that depends on interest rates, bank liquidity, debt yield requirements, and market valuations is structurally vulnerable.

There is an additional dimension: when a cash-out refinancing pushes leverage back toward high loan-to-value levels, the safety margin for investors shrinks. Downside risk increases, while the IRR appears more attractive on paper. The metric improves – the risk structure does not necessarily follow.

A robust multifamily investment is therefore not defined by the highest modeled IRR, but by its stability under stress conditions. It should hold up even if interest rates remain elevated, cap rates expand, or lending standards tighten.

Refinancing can be a meaningful strategic lever. It must never, however, be the prerequisite for an investment to be economically viable.

How We Evaluate Refinancing Assumptions

We do not categorically reject refinancing projections. What matters is whether they represent an optional optimization or a structural prerequisite for the investment to function. This distinction is at the heart of our analysis.

There are scenarios in which a refinancing is both reasonable and defensible. One example from our own practice involved a project where we assumed a long-term fixed financing at a rate below 3%, with approximately 30 years of remaining term. The capital structure was stable, operational risk was low, and ongoing cash flow was viable independent of any refinancing. Even if a planned refinancing had proven unachievable at a later date, the result would have been a delay in capital return – not a compromise of the investment’s economic stability. In such cases, refinancing functions as a strategic option, not a necessary condition.

Our review therefore always begins with a simple but revealing step: we remove the refinancing entirely from the model. If the investment still generates an adequate equity multiple and an acceptable IRR at the planned exit, the return is primarily driven by operational value creation. If the return deteriorates significantly, it becomes clear that the refinancing is a load-bearing pillar of the calculation – and therefore a structural risk.

In the next step, we subject the refinancing itself to rigorous stress testing. We model higher interest rates, more conservative cap rates, lower loan-to-value ratios, and tighter lending standards. We analyze debt yield and DSCR in particular, as these metrics represent the key risk guardrails from a lender’s perspective. Even moderate changes in rate levels or valuations can substantially reduce the maximum supportable loan amount.

We also examine the capital structure following a potential cash-out refinancing. If the loan-to-value is pushed back toward high leverage levels, the safety margin for investors narrows considerably. The IRR may increase on paper, but sensitivity to NOI declines, valuation adjustments, or liquidity constraints increases in parallel. An aggressive capital return can therefore significantly amplify downside risk.

An additional consideration is covenant structure. Even when a refinancing is formally executed, tightened DSCR or debt yield requirements can lead to cash traps, where distributions are restricted or halted entirely. For investors, this means: the asset continues to operate, but without freely distributable cash flow. This scenario must be factored into the underwriting.

Finally, valuations themselves carry inherent uncertainty. Appraisers work within ranges for market rents, vacancy, and cap rates. Even minor adjustments can materially affect the appraised value. Refinancing viability is therefore not solely a function of NOI – it is equally a matter of conservative valuation assumptions.

Institutional underwriting approaches refinancings not as return accelerators, but as structural interventions in the capital architecture. A refinancing makes sense when it optimizes an already robust investment. It becomes problematic when it is relied upon to create that stability in the first place.

Context Matters More Than Ever

Recent years have demonstrated clearly how rapidly capital market conditions can shift. Multifamily deals structured in 2020 and 2021 were frequently built on assumptions of persistently low interest rates, abundant liquidity, and stable or declining cap rates. Under those conditions, refinancing projections were treated as near-certainties.

The rapid rate cycle beginning in 2022 fundamentally changed the environment. Rising financing costs, tighter lending standards, and cap rate expansion rendered many refinancing assumptions unachievable. In practice, this resulted in loan extensions, preferred equity raises, additional capital calls, or reduced distributions.

This was not an anomaly – it was a textbook capital market cycle. Interest rates, liquidity, and valuation levels do not move linearly; they follow cyclical patterns shaped by monetary policy, inflation, and macroeconomic conditions. Periods of exceptionally favorable financing are just as temporary as periods of restrictive credit. Underwriting a refinancing under boom conditions implicitly assumes that those exact conditions will persist at the critical moment.

There is also a procyclical effect to consider: in expansionary market phases, NOI, valuations, and loan-to-value ratios often rise simultaneously while lending standards loosen. Refinancing models appear especially plausible in such environments, because multiple positive factors are operating in concert. When the cycle turns, these effects tend to reverse just as simultaneously. Rising rates, declining valuations, and tighter credit standards reinforce one another – precisely when a refinancing is needed most.

Professional underwriting must therefore account not only for operational risks, but explicitly for cyclicality. The defining question is not how an investment performs in the base case scenario, but how it holds up in a more restrictive financing environment. Anchoring a refinancing as a core assumption inevitably embeds a macro forecast into the return structure. That is legitimate – but it demands particular rigor and conservative scenario planning.

Refinancings are not inherently problematic. They become problematic when their viability depends on sustained, supportive capital market conditions. A sound investment thesis must hold up under less favorable market conditions as well.

A Balanced Perspective

Refinancings are not an inherently flawed instrument. In certain constellations, they can represent a sound strategic option – particularly when initial leverage is conservatively structured, the operational path to sustainable NOI growth is clearly defined and measurable, and the capital structure remains stable without interim refinancing. In such cases, refinancing functions as an additional lever, not a load-bearing foundation.

What matters, however, is the framing. A refinancing may optimize a strong deal – it must not stabilize a weak one. When the economic viability of an investment is established only through favorable debt conditions, the return is not primarily a function of operational performance. It is a function of an implicit market forecast.

For investors, this means distinguishing between nominal IRR and structural quality. A high projected IRR can be the result of early capital returns or aggressive leverage, without any improvement in the underlying substance of the investment. What matters is therefore not the magnitude of the metric, but its derivation. Returns grounded in sustainable cash flow, conservative financing, and realistic exit assumptions are fundamentally different from returns that depend on interest rate sensitivity, valuation assumptions, or capital market timing.

There is a further dimension: the quality of an investment reveals itself not in the base case scenario, but in its resilience under stress. How does the asset perform under stagnant rent growth? How does the capital structure respond to rising financing costs? What is the buffer between actual and minimum required debt service coverage? These questions matter more than any modeled upside scenario.

Long-term wealth creation is not built on optimism – it is built on risk discipline. Confidence is earned through transparency of assumptions, conservative structuring, and the willingness to forego seemingly attractive levers when they compromise stability.

Protecting the downside first is the foundation for sustainable returns.