In conversations with wealthy families, one question almost always sits in the room: How can what one generation has built be preserved?

The intuitive answer is often simple: once wealthy, always wealthy. Reality is far less comfortable.

Wealth preservation across generations is not the normal case. It is the exception. Large fortunes disappear more often than public debate suggests — not only through war, revolution or expropriation, but through decisions that appear reasonable at the time: excessive withdrawals, insufficient diversification, weak cost structures, family fragmentation and, above all, concentrated entrepreneurial risk.

Victor Haghani and James White describe this dynamic powerfully in their book “The Missing Billionaires”. Their thought experiment appears sober at first. On closer inspection, it challenges one of the central assumptions held by many wealthy families: that wealth, once created, primarily needs to be administered.

That is not true.

Creating wealth and preserving wealth are two different tasks. They require different mindsets, different levels of risk tolerance and different structures.

Where Did the Billionaires Go?

Haghani and White begin with a simple historical observation. Around 1900, the United States had roughly 1,000 households with wealth of at least five million dollars. At the time, that was not upper-middle-class prosperity. It was the absolute top of the American wealth pyramid.

Depending on the benchmark used, that sum translates into very different figures today. Adjusted for inflation, it falls in the high hundreds of millions. Measured by economic significance, relative purchasing power or share of total wealth at the time, it can be placed much higher. The exact conversion is not the point. The point is this: these families belonged to the financial elite of their era.

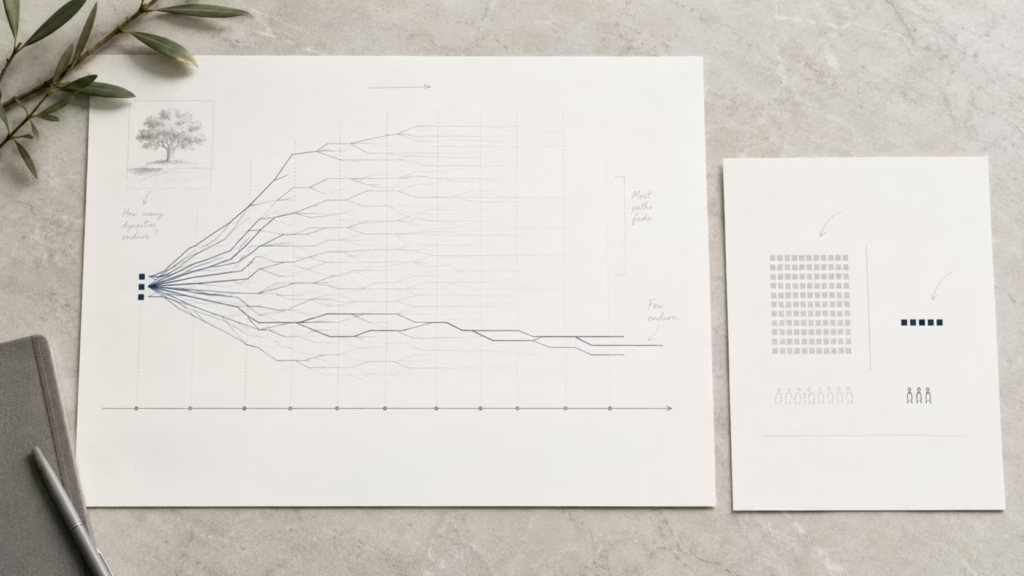

Haghani and White then ask a sober question: What would have happened if those families had invested their wealth broadly in U.S. equities, withdrawn only two percent per year in real terms and minimized taxes through a disciplined buy-and-hold strategy?

The result is striking. From the roughly 1,000 starting families, several thousand billionaire families could have emerged by 2022 — accounting for family growth and the splitting of assets across descendants. Haghani and White estimate this hypothetical group at about 4,300 families, each with at least roughly 2.3 billion dollars in wealth.

Reality looked different. In 2022, the United States had far fewer billionaire families. More importantly, the analysis shows that there is hardly any visible dynastic continuity between the ultra-rich families of 1900 and today’s billionaire families.

This is where the term “Missing Billionaires” comes from. It refers to fortunes that, under simple assumptions, should have survived — but in reality disappeared.

That is the uncomfortable finding: large fortunes do not disappear only through historical catastrophes. They also disappear through withdrawals, costs, taxes, inheritance division, family dynamics and poor capital decisions.

For wealth preservation, this is a central lesson. Wealth does not protect against capital loss. It only increases the responsibility to manage risk deliberately.

Historical Evidence: The Vanderbilts

The Vanderbilt case makes the thought experiment by Haghani and White historically tangible.

Cornelius Vanderbilt died in 1877 as one of the richest men of his time. His wealth was not built through broad diversification, but through control over transportation routes: first steamboats, later railroads, connections, pricing and access. Vanderbilt did not build a portfolio. He built power over infrastructure.

That logic was extraordinarily effective for creating wealth. For preserving wealth across several generations, it was not a sufficient structure.

The scale of that family fortune can still be seen today in North Carolina. Biltmore Estate, built by George Washington Vanderbilt II, is considered the largest private residence in the United States. The house comprises roughly 16,600 square meters of living space; the original estate covered around 50,600 hectares — about 506 square kilometers. That made it larger than many major German cities and more than half the size of Berlin.

Standing there, one does not merely see a large house. One sees the material trace of a family fortune that once financed an entire world of its own.

A little more than a century later, little remained of that financial power. At a family reunion in 1973, around 120 direct descendants of Cornelius Vanderbilt came together. Among them, not one was a millionaire.

That is what makes the story so instructive: the Vanderbilt fortune did not disappear through one single disaster. It disappeared through a long chain of inheritance division, consumption, poor allocation, lack of discipline and weak institutional structure.

The name remained. The fortune did not.

For family wealth, this is the decisive lesson: size does not protect. A famous founder does not protect. Prestige does not protect. Wealth preservation does not come from origin. It comes from structure, discipline and risk control.

Nelson Bunker Hunt: When Wealth Protection Becomes a Bet

Nelson Bunker Hunt is the counterpoint to Vanderbilt. In his case, wealth destruction did not take four generations. It largely unfolded within a single lifetime.

Hunt came from one of the great Texas oil families. His father, H.L. Hunt, had built the family fortune in the oil business. Nelson Bunker Hunt inherited capital, access, creditworthiness — and a way of thinking in large dimensions.

In the 1970s, silver became his answer to a world he no longer trusted. Inflation, the oil crisis, a weaker dollar, distrust of paper money: Hunt did not see silver as merely a commodity. He saw it as protection against the debasement of money.

Together with his brother Herbert, he bought physical silver and built large positions through futures. The strategy was simple and risky at the same time: control enough silver that the market price could no longer be thought of independently of the Hunts.

At first, the logic worked. The silver price rose from around six dollars per ounce in early 1979 to almost fifty dollars in January 1980. On paper, a conviction turned into billions.

Then it was not Hunt’s opinion that changed first. It was the market environment.

COMEX tightened the rules in early 1980. New large long positions were restricted, margin requirements were increased, and parts of the market later became “liquidation only”: positions could be reduced, but no longer expanded. For normal investors, that is a rule change. For someone whose strategy depends on size, credit and continued buying pressure, it is a structural break.

From that moment on, the market worked against the Hunts. The silver price began to fall. With every decline, the collateral securing their loans weakened. At the same time, margin calls increased. Banks became more cautious. Credit became tighter. What had been intended as protection against paper money suddenly depended on exactly what Hunt distrusted: liquidity, credit lines and the confidence of the financial system.

On March 27, 1980, later known as “Silver Thursday”, the situation tipped. The Hunts could no longer meet margin calls. Silver fell sharply that day — not because silver had become worthless overnight, but because a leveraged, concentrated position was forced into a market with no additional buyers and where credit had suddenly become the scarcest resource.

That is the decisive point: Hunt was not entirely wrong about inflation risk. He was wrong about the structure. A real risk was answered with a strategy that was too concentrated, too leveraged and too illiquid.

For wealth preservation, this is a hard lesson. Protecting wealth must not be confused with controlling a market. And conviction must never become so large that it consumes the very liquidity needed to survive.

René Benko: When Real Estate Becomes a Credit Machine

René Benko, born on May 20, 1977 in Innsbruck, did not begin with a finished real estate empire. His first steps were small: attic conversions, refurbishments, project development. In 2000, he founded Immofina, which later became Signa. The rise did not come from one single asset, but from a method: develop projects, attract investors, buy larger assets, increase valuations, raise new capital — and finance the next step.

That is how Signa gained access to names everyone recognized: KaDeWe in Berlin, the Golden Quarter in Vienna, stakes in the Chrysler Building in New York, Selfridges in the United Kingdom, and the planned Elbtower in Hamburg. These were not trophies on the side. They were part of the system. Visible premium assets create trust. Trust creates financing. Financing creates growth.

The mechanism behind it was not difficult to understand, but highly sensitive. Income-producing commercial real estate is valued, at its core, on the basis of its earnings. What matters is therefore not only how attractive a building is or how prominent its address sounds. What matters is the rent it carries, how stable those rents appear, and at what rate those earnings are capitalized.

This is where the power of the model lay. Higher rents support higher real estate values. Higher real estate values create more collateral. More collateral enables more debt. More debt enables new acquisitions and new projects. Real estate ownership becomes a credit machine.

At Signa, there was an additional sensitive point: real estate and retail were partly intertwined. The group held prominent department store properties and was also connected to retail businesses such as Galeria and the KaDeWe Group. Critics alleged that high lease agreements supported real estate valuations. Signa rejected these allegations. The structural point remains important: if retail space has to carry high rents, that can strengthen the property value in the short term — but weaken the operating tenant over the long term.

From the outside, this looked like strength for a long time. Structurally, it was a bet: on permanently cheap money, high valuations, resilient rents, refinanceable debt and investor confidence. As long as those factors moved in the same direction, the model appeared almost unassailable.

Then the price of money changed.

From 2022 onward, interest rates rose quickly. That did not merely make financing more expensive. It reversed the entire mechanism. Higher rates depress property valuations. Lower valuations weaken collateral. Weaker collateral makes refinancing harder. At the same time, ongoing projects continue to require capital. And operating tenants that were already under pressure do not become more stable through high rents.

At the end of November 2023, Signa Holding filed for insolvency. Other companies within the Signa complex followed. In 2024, Benko himself filed for insolvency as an entrepreneur. In 2025, he was arrested; Austria’s economic and corruption prosecutors are investigating several matters. Benko denies the allegations and has appealed convictions.

For wealth preservation, the Benko case is so instructive for one reason: it does not show that real estate is a poor asset class. It shows that real estate can become dangerous in the wrong structure.

Bunker Hunt bet on silver against paper money. Benko bet on real estate values, rents, credit and permanently cheap money. The instrument was different. The pattern was similar: strong conviction, high concentration, growing dependence on financing — and an assumption that eventually stopped holding.

A good asset does not protect wealth if the structure behind it is fragile. Wealth preservation does not begin with the prestige of an address. It begins with cash flow, debt, maturities, liquidity reserves and the ability to remain in control when the market stops cooperating.

Forbes 400: The Top Is Not a Closed Club

Anecdotes explain the mechanics. Lists show whether the pattern holds more broadly.

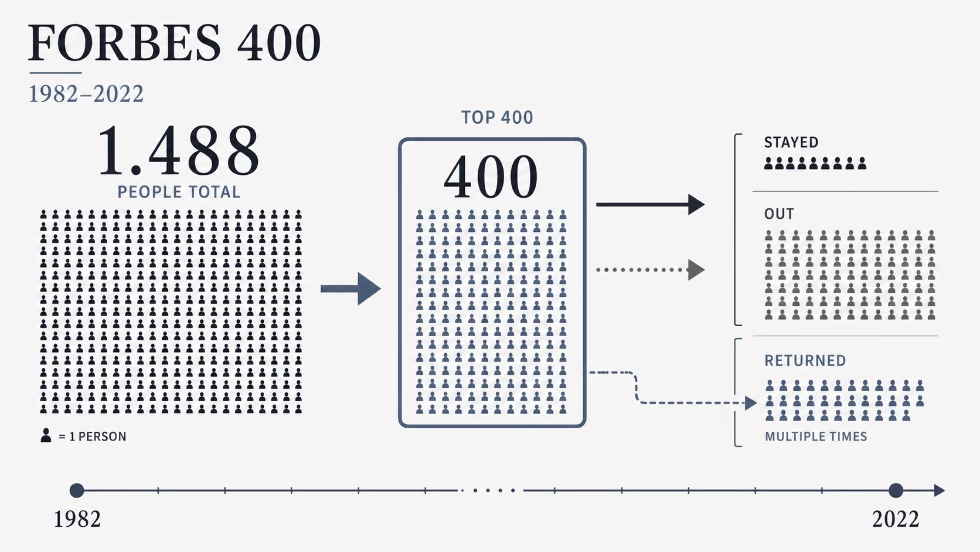

The Forbes 400 list was first published in 1982. Each year, it records the 400 richest Americans. Looking only at the aggregate wealth, one sees mainly this: the top has become substantially richer over decades. Looking at the names, however, shows something else: they are not the same people.

In 2022, only 17 people from the first Forbes 400 list of 1982 were still on the list. Put differently: more than 95 percent of the original individuals were no longer represented four decades later.

That is the decisive point. The wealth elite grows as an aggregate. But its composition changes constantly. New entrepreneurs rise. Old fortunes fall back. Industries change. Families branch out. Valuations shift. Anyone who looks only at “the rich” as a statistical group misses the movement within that group.

Korom, Lutter and Beckert conducted an academic analysis of Forbes 400 data from 1982 to 2013. Their dataset includes 1,488 individuals who appeared at least once among the 400 richest Americans during that period. Most did not remain on the list permanently. Many dropped out once, some repeatedly. At the same time, the study shows that inherited family wealth increases the likelihood of remaining on the list for longer. Old fortunes do not disappear automatically. But they do not automatically remain at the top either.

This distinction matters. The argument is not that wealth is fleeting and everything disappears immediately. The argument is that wealth is more dynamic than public debate often suggests. The top is not a closed club of permanent fortunes. It is a competition for capital, market position, structure and timing.

Arnott, Bernstein and Wu reach a similar conclusion in their study “The Myth of Dynastic Wealth”. Viewed as families, the rich often do not become ever richer after the creation of a large fortune. Across generations, they frequently become relatively poorer. A significant share of top-level wealth at any given point is newly created wealth — not merely inherited capital from old dynasties.

This overturns the popular narrative. “The rich get richer” is only true when “the rich” are treated as an abstract group. For concrete families, something else applies: wealth has to be defended, structured and realigned again and again.

For wealth preservation, this is the central message. Owning a large fortune does not automatically make a family a stable dynasty. It places that family in a long line of families that overestimated precisely that stability.

Are the Rich Really Getting Richer?

The precise answer is: as a group, often yes. As concrete families, much less often.

This is where much of the imprecision in debates about wealth begins. “The rich” are treated as if they were a fixed group with stable membership. In reality, it is usually a statistical category. People enter it. Others fall out. Family fortunes are split, consumed, poorly invested, overleveraged or lose their economic foundation.

That changes the meaning of the sentence significantly. A rising share of wealth held by the top one percent can be statistically correct. But it does not follow that the same families become ever richer across generations. For wealth preservation, precisely this distinction is critical.

Public perception reinforces the distortion. Large success stories are visible: IPOs, rankings, founder portraits, entrepreneur biographies, conferences. The loss of large fortunes unfolds differently. It takes place through inheritance divisions, estates, bank negotiations, sales, restructurings, divorces, tax questions and quiet family decisions. There is rarely a stage for that.

This creates the impression that wealth is more stable than it often is for individual families. What is visible are the fortunes that are newly created or still present. Less visible are those that have disappeared from the top.

A similar issue appears in the debate about global inequality. The global Gini coefficient, a measure of income inequality, has not risen since 1990; it has fallen. The main reason lies in the economic rise of large emerging markets, especially China and India. In those countries, incomes grew faster than in many industrialized economies.

This does not mean inequality is irrelevant. It also does not mean all countries have become more equal. Inequality can rise within individual countries while global income inequality falls. Both can be true at the same time.

That is why the blanket formula “the rich get richer” is analytically too crude. It confuses groups with families, income with wealth, national developments with global developments and statistical shares with actual wealth biographies.

For wealth preservation, a sober point follows: a large fortune is not an end state. It is a condition that requires structure. Without withdrawal discipline, diversification, liquidity, tax planning, governance and risk limitation, even very large capital can disappear over time.

The better question is not whether “the rich” keep getting richer. The better question is: Which structures prevent created wealth from disappearing again?

The Seven Causes of Wealth Erosion

Large fortunes rarely disappear because of a single mistake. In most cases, several forces operate at the same time: family, taxes, costs, withdrawals, illiquidity, emotions and poor entrepreneurial decisions. Some work over decades. Others hit the capital base in a short period of time.

Haghani and White describe seven recurring causes.

At the beginning stands the simple mathematics of inheritance division. A concentrated fortune is distributed among children, later among grandchildren and additional family branches. One large block becomes several smaller units. Each unit needs its own withdrawals, its own liquidity and its own planning. Even without poor investment decisions, the original fortune loses economic force.

Divorces intervene at a different point. In entrepreneurial families, real estate wealth or illiquid holdings, the issue is not merely a mathematical division. It is valuation, control and liquidity. Illiquid wealth comes under particular pressure when settlement claims cannot be met from current resources. Sales then arise not from strategic conviction, but from necessity.

Taxes work more quietly, but persistently. Income taxes, estate taxes, gift taxes and possible wealth taxes do not destroy capital through drama, but through repetition. They increase the demands on structure, holding periods, withdrawals and liquidity planning. Wealth without order pays a price for that.

Lifestyle spending reaches directly into substance. What matters is not the absolute level of spending, but its relationship to the expected real return of the wealth.

If annual withdrawals remain sustainably below that return — for example at two percent in real terms — the capital base remains intact and continues to work. If withdrawals are materially higher — for example five or ten percent of wealth per year — the family is no longer living from returns, but from the substance itself.

Over decades, this difference leads to entirely different outcomes: growing capital in one case, gradually consumed capital in the other.

Costs are among the underestimated opponents of wealth preservation. Management fees, performance fees, transaction costs, administrative expenses and advisory fees often appear acceptable in isolation. In aggregate, however, they hit the decisive point: net return after costs, taxes and inflation. A persistently high cost block reduces the ability of the wealth to carry withdrawals, inflation and tax burdens over decades.

Philanthropy follows its own logic. Foundations and donations are expressions of responsibility, conviction and social impact. In wealth accounting, they remain capital transfers. Money permanently dedicated to a foundation, a purpose or a charitable structure is no longer available to the family as freely deployable wealth. This is not an argument against philanthropy. It is an argument for clarity: social impact and dynastic wealth preservation are two different objectives.

The most dangerous cause lies in poor entrepreneurial investments.

That is where slow erosion ends. A major wrong decision does not hit the edge of a fortune, but its core. Inheritance division, taxes, costs and lifestyle spending weaken capital gradually. A concentrated entrepreneurial mistake can destroy it much faster.

This is where the conflict between wealth creation and wealth preservation becomes visible. Large fortunes are often created through concentration: a company, an industry, a real estate thesis, a market cycle, a founder’s decision. Creation rewards focus, courage and scale. Preservation later requires limitation, diversification, liquidity and distance from one’s own success story.

The qualities that create a fortune do not automatically preserve it. After creation, a different task begins.

The Core Problem: Concentration Risk After Wealth Creation

The decisive conflict begins where wealth creation was successful.

Large fortunes are often not created through broad diversification. They are created through concentration: a company, an industry, a real estate thesis, a market cycle, a technological development, an entrepreneurial conviction. Capital, attention and risk are focused on one point. That is often how extraordinary wealth is created.

For creating wealth, this concentration is often the prerequisite. For preserving it, it later becomes the danger.

After wealth has been created, the task changes. It is no longer about turning little capital into a great deal of capital. It is about keeping existing capital effective and available over decades. That task requires a different logic: less dependence on a single assumption, more liquidity, more diversification, more protection from one’s own success pattern.

Many families find this transition difficult. The reasons are not only financial, but also psychological. The company, industry or investment thesis that created the wealth is not just another asset. It is part of the family story. It stands for competence, courage, status, identity and control. Other asset classes often appear defensive, boring or like a vote of no confidence in the family’s own origin.

This is where the risk emerges. The first generation learned: concentration creates wealth. The next generation often unconsciously adopts the wrong conclusion: concentration preserves wealth.

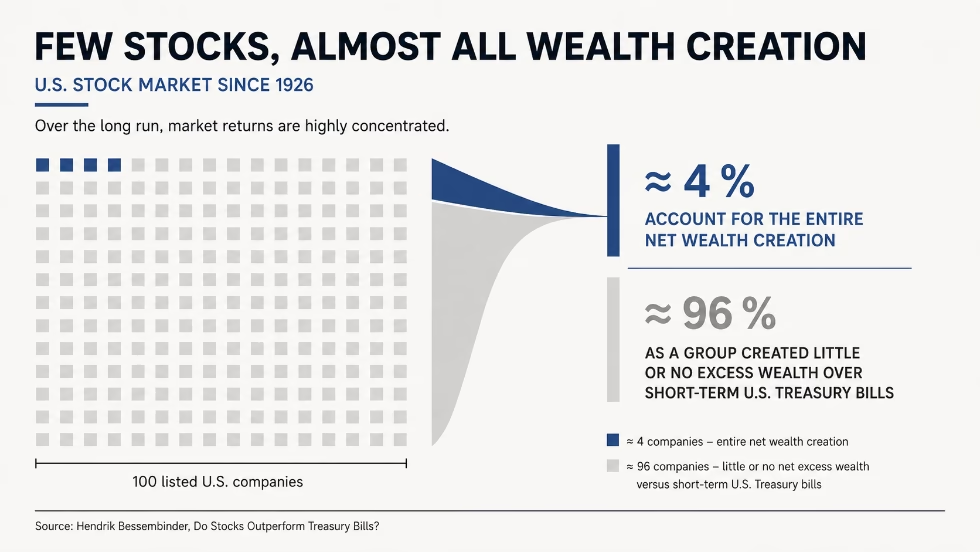

Capital market research shows why that conclusion is dangerous. Hendrik Bessembinder examined how much wealth individual U.S. stocks have actually created since 1926. The result is unusually clear: the long-term wealth creation of the U.S. stock market came almost entirely from a small minority of exceptional companies.

The best roughly four percent of listed U.S. companies explained the entire net wealth creation of the market since 1926. The remaining stocks were not all worthless. Many were solid, some were successful, some were weak, some disappeared. But as a group, they created little additional wealth relative to short-term U.S. Treasury bills.

That is the decisive point: the stock market as a whole was very successful because a small share of companies was extremely successful. A broadly diversified investor owns those few winners automatically. A concentrated investor has to identify them in advance, hold them, and avoid the many wrong candidates.

In hindsight, great winners look obvious. Beforehand, they are not.

For entrepreneurial families, this finding is especially important. A single company can be the source of a large fortune. The same company can later remain the largest threat to that fortune if too much capital, too much identity and too much future remain tied to it.

Wealth preservation does not require a break with one’s own history. It requires distance from it. The success story of wealth creation must not become the next generation’s investment strategy without review.

The Old Pattern: Three Generations

There are old formulas for this pattern. Otto von Bismarck is credited with the sentence: “The first generation creates wealth, the second manages it, the third studies art history and the fourth degenerates.” The Anglo-American saying is shorter: “From rags to riches and back again in three generations.”

There is also a commonly told variant in the Arab world: the grandfather rode a camel, the father did as well, the son drives a Mercedes, the grandson a Land Rover — and the great-grandson is back on the camel. The precise attribution is uncertain. The idea is still powerful because it describes the same experience in a different imagery: creation, prosperity, habituation, loss.

Such sentences do not replace data. They describe a pattern observed across many cultures: wealth is created, then managed, then taken for granted. That is where the risk begins.

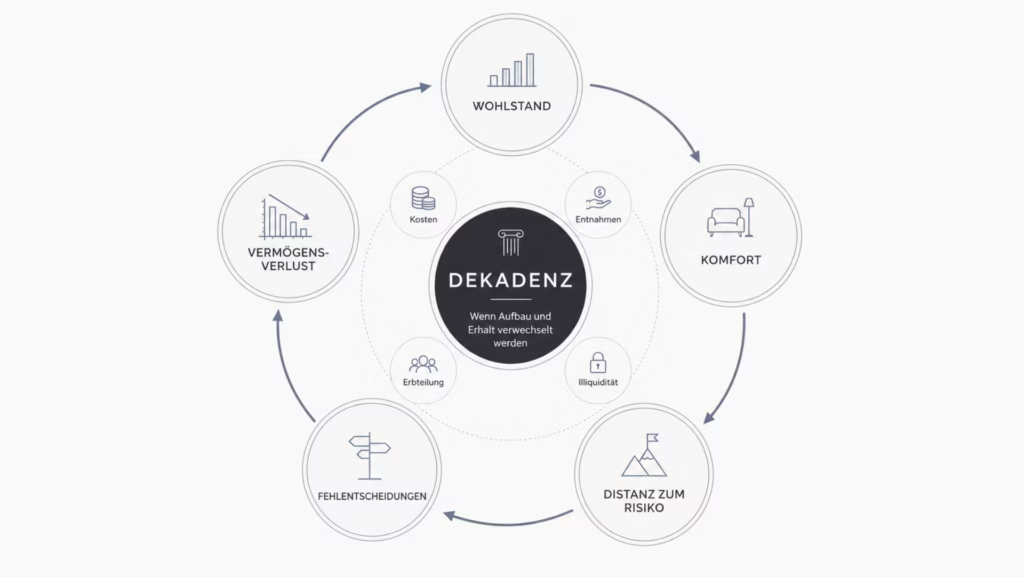

Alexander Demandt sharpened a concept for historical processes of decline that is helpful here: decadence. It does not simply mean luxury or extravagance. It describes a condition in which external forms still exist while the inner carrying capacity declines.

The institution, the name, the house, the rituals and the rank remain visible. But the ability to bear risk, make decisions and renew substance becomes weaker.

Applied to family wealth, this is a precise image. The third generation does not fail because grandchildren are automatically weaker than founders. That explanation is too convenient. The third generation faces a different structure. It inherits not only capital, but also history, expectations, roles, family branches and symbols. Wealth is no longer merely an economic resource. It is origin.

This is where the psychological tension lies. The original company, property or industry stands for competence, status, memory and family identity. In family business research, this non-financial value is described as “socioemotional wealth”. Families hold on to control, name, influence and tradition because these things mean more to them than a pure return metric.

This explains many decisions that look unreasonable from the outside. A company remains in the family although a sale would make economic sense. A family member receives responsibility although an external manager would be better suited. An industry remains overweight because it belongs to the family story. Diversification is not understood as risk control, but as distance from the founder.

That is how decadence arises in a wealth-strategy sense: not through champagne, art or beautiful houses, but through the loss of the ability to treat wealth as a task.

Thomas Mann’s “Buddenbrooks”, one of the great social novels of German literature, describes precisely this transition. At the beginning stands commercial discipline. Later, attention shifts: representation, rank, culture, fatigue, family expectations. The novel is not an economic study. But it shows how wealth loses its sustaining attitude while façade, name and self-image continue to exist for a while.

That is the decisive point. The third generation is not the problem. The problem is a family that still understands wealth as origin, but no longer organizes it as responsibility.

Wealth preservation across generations therefore does not arise from nostalgia. It arises from governance, role clarity, withdrawal rules, professional leadership, diversification and the willingness not to confuse family identity with capital allocation.

The Consequence: Wealth Preservation Is Structural Work

After all these examples, what remains is not a technical point, but a strategic one: wealth preservation begins with a change of role.

The creation of large fortunes often follows a logic of concentration. Capital, attention, risk and decision-making power are focused on one point: a company, an industry, a real estate thesis, a market cycle, a technological development. Without that concentration, many large fortunes would never be created.

But this logic does not automatically carry into the next phase. After wealth has been created, the task is no longer to generate extraordinary jumps in wealth through high concentration. It is to keep existing capital effective and available over decades. That requires withdrawal discipline, cost control, tax structure, liquidity, diversification, governance and a clear understanding of which risk is being paid for — and which risk is merely being carried out of habit.

The real difficulty is not theoretical. The theory is comparatively simple. Wealth must not remain permanently dependent on one single assumption. Implementation is harder because families have to limit the very logic that made them wealthy.

Emotionally, that can feel like distancing oneself from one’s own origin. In truth, it is protection. The act of creation is not devalued when the wealth is structured differently afterward. It is taken seriously.

Haghani and White describe this transition as the shift from wealth creator to wealth preserver. These roles are less similar than many families assume.

- Creation rewards focus, courage, speed and the ability to withstand great uncertainty.

- Preservation requires different qualities: patience, limitation, liquidity discipline, cost awareness and the willingness not to pursue every attractive opportunity.

This is not a rejection of entrepreneurship. It is a rejection of the belief that every successful creation logic automatically becomes the right preservation logic. Entrepreneurial judgment remains important. But it has to be embedded in a different architecture: risk budgets instead of reflexes, governance instead of family feeling, cash flow instead of prestige, structure instead of memory.

This is the lesson of the Missing Billionaires. The Vanderbilts, Bunker Hunt, René Benko, the Forbes 400 data and the old pattern of the third generation do not tell the same story because the assets were the same. They tell the same story because the structure was similar: high concentration, strong conviction, too little limitation and too much trust that a successful past would also carry the future.

That assumption is dangerous.

Once wealthy, always wealthy — that is not a law of nature. It is a comfortable story. Wealth preservation does not arise from size, origin or prestige. It arises from decisions that often look unspectacular: less debt, longer maturities, lower costs, disciplined withdrawals, better governance, sufficient liquidity, broader risk diversification and the willingness not to confuse a good story with a good structure.

The connection to Whitestone lies precisely here.

Serious capital allocation does not begin with the question of which asset sounds attractive today. It begins with the question of which structure still holds when the original success story no longer does.

For us, this is the core of every investment decision. Not prestige. Not size. Not the hope that a market will simply continue to rise. But cash flow, risk control, liquidity, costs, debt and the sober assessment of whether an investment still works under pressure.

Wealth is built through opportunities. It is preserved through structure.