Nearly half of the Americans surveyed consider investors one of the main causes of high housing costs. In a nationwide survey conducted in 2025, 48 percent identified investors who buy housing for profit as a major driver of prices.

The survey, however, refers to investors in general. In the public debate, that quickly becomes “Wall Street”: small landlords, local LLCs, house flippers, and large institutional platforms are grouped into a single category.

This is where the problem begins. Institutional investors are neither responsible for every development in the U.S. housing market nor inherently without influence. What matters is their actual market share, local concentration, and business model.

We examined eleven common claims—using the available data, without simplistic blame and without defending institutional owners across the board.

Myth 1: Institutional Investors Buy 25 Percent of All Homes for Sale

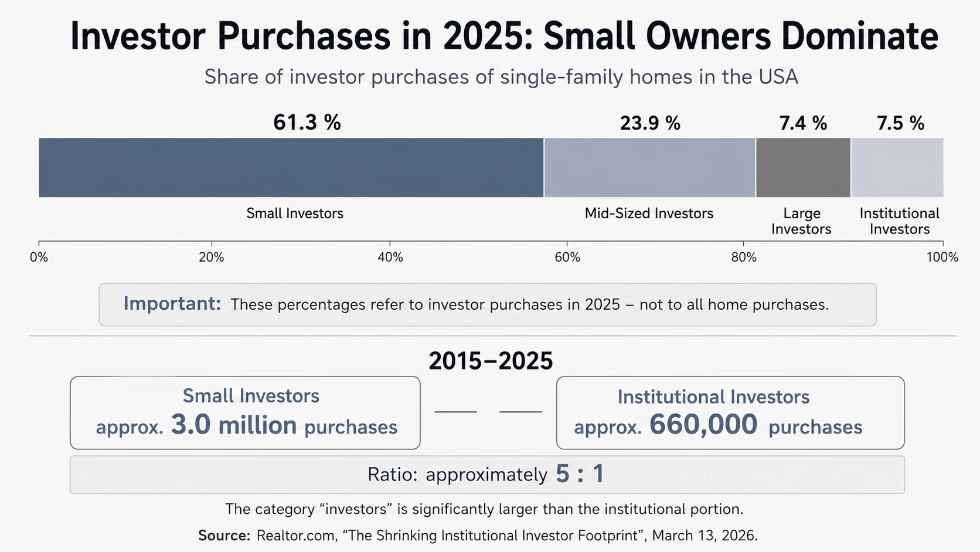

The confusion begins with the terminology: Many people use “investors” and “institutional investors” interchangeably. Market statistics, however, also classify private landlords, house flippers, and local companies as investors. The overwhelming majority of these purchases are made by smaller operators—not Wall Street.

Realtor.com estimates that, between 2015 and 2025, small investors made about 3.0 million purchases, compared with roughly 660,000 purchases by institutional investors. Small investors therefore bought approximately five times as many single-family homes as institutional buyers. In 2025, they accounted for just over 61 percent of investor purchases; institutional buyers accounted for 7.5 percent.

The sales side matters too: BatchData reported that large portfolio owners sold 5,801 homes and bought 4,069 in the second quarter of 2025. They were therefore net sellers for the sixth consecutive quarter.

A nationwide ban on institutional purchases would almost eliminate institutional acquisitions. It would, however, do little to change the broader shortage and affordability of housing.

The 25 percent claim arises mainly because very different buyer groups are lumped together.

Myth 2: Without Institutional Buyers, SFR Renters Would Become Homeowners

An institutionally purchased home is not automatically a lost homeownership opportunity. This assumption overlooks the fact that most investor purchases are made by smaller owners. Investors also frequently buy homes that require renovation, capital, and financial flexibility—not necessarily properties that traditional owner-occupiers would have purchased immediately.

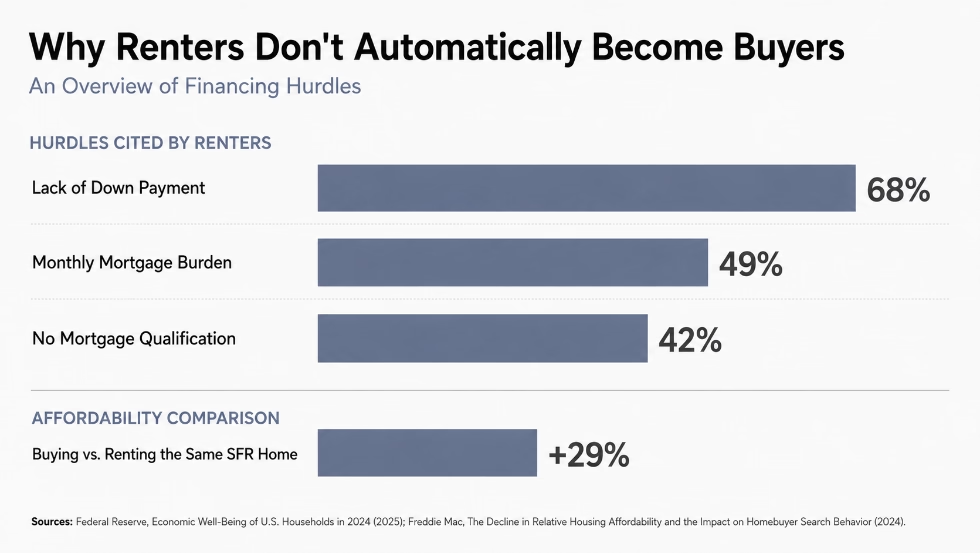

The more important point is this: A renter does not automatically become a buyer simply because an institutional bidder disappears. To purchase a home, a household needs a down payment, sufficient creditworthiness, and enough ongoing income to cover the mortgage, property taxes, insurance, and maintenance.

The Federal Reserve makes these hurdles clear: In 2024, 68 percent of renters cited the lack of a down payment as a reason for continuing to rent. Forty-nine percent cited the monthly mortgage payment, and 42 percent said they would not qualify for a mortgage.

Even within the single-family rental segment, the direct move into homeownership is not the norm. A survey of SFR renters found that fewer than one in five would try to buy a home if the single-family home they rented were unavailable. Many would instead rent an apartment or live with family and friends.

Higher interest rates widen this gap. Freddie Mac estimated in September 2024 that the median monthly cost of buying the same rented single-family home would have been 29 percent higher than the rent.

A ban on institutional buyers could change individual bidding situations. It would not turn renters into mortgage-qualified buyers. Access to homeownership usually fails not because of a single buyer group, but because of prices, financing, and down-payment capital.

Myth 3: Institutional Buyers Drive Up Home Prices

Institutional buyers can influence prices. Every additional buyer matters in a supply-constrained market. The question, however, is not whether there is an effect. The question is whether institutional investors are the central reason home prices are high.

There is little robust evidence for that. Freddie Mac attributed the sharp post-pandemic increase in home prices primarily to low mortgage rates, insufficient supply, demographic demand, and migration into already tight markets. Investors were not among the main drivers.

That does not fully absolve institutional buyers. Joshua Coven finds measurable price effects where institutional investors were particularly active. This is the proper distinction: The effect is real, but it is not the principal national driver.

The period after the financial crisis also shows how much context matters. At the time, institutional investors bought many distressed homes in markets where private buyers were absent. The Philadelphia Fed describes how, from 2007 to 2014, these purchases supported local price recovery while weighing on the homeownership rate.

The balanced conclusion is therefore: Institutional buyers can produce local price effects. The broader explanation for high home prices, however, remains limited housing supply, expensive financing, and strong regional demand.

Myth 4: Institutional Investors Win Bidding Wars with All-Cash Offers

A cash offer is not automatically an institutional offer. In the U.S. housing market, wealthy owner-occupiers, repeat buyers, second-home buyers, private investors, and flippers also purchase without conventional financing. NAR reported for 2025 that 26 percent of all buyers paid cash.

Institutional SFR buyers also follow a different logic from private owner-occupiers. Their purchase price must fit the achievable rent, renovation costs, financing, and return requirements. An inflated price does not make a home a better investment.

This helps explain why many investors do not necessarily compete for the same properties as traditional first-time buyers. Freddie Mac found that institutional and smaller investors often buy discounted homes with greater repair needs. Such properties are frequently harder for owner-occupiers to finance and require additional renovation spending. In 2020, half of institutional purchases fell below the bottom price quartile paid by first-time buyers.

That does not mean there is no competition. In tight local markets, an institutional buyer can outbid individual owner-occupiers. That is not the same as saying institutional investors systematically push ordinary buyers out of the market through all-cash bids.

Myth 5: Institutional Investors Buy Up Affordable Starter Homes

A low purchase price does not automatically make a home a conventional first-time-buyer property. Homes are often inexpensive because they need repairs, are harder to finance, or require additional renovation capital.

Freddie Mac found in 2022 that institutional and smaller investors often buy homes below market value that require more repairs than many first-time buyers are willing or able to undertake. In 2020, half of institutional purchases fell below the bottom price quartile paid by first-time buyers; in 2021, this was still two out of five purchases.

Professional buyers can price such properties more easily. The Urban Institute points to the significantly larger renovation budgets of major SFR providers and to a financing advantage: Institutional buyers can often structure the acquisition and renovation separately from conventional purchase financing. Owner-occupiers, by contrast, rely more heavily on mortgages that do not always accommodate major renovations effectively.

This is not an acquittal. Joshua Coven shows that institutional buyers in his sample also purchased directly from owner-occupiers. There is therefore genuine competition for individual homes.

The blanket claim nevertheless remains too simple. Institutional investors do not merely take “starter homes” away. They often buy homes that appear affordable to first-time buyers but in practice carry repair, financing, and down-payment risks.

Myth 6: Institutional Investors Let Homes Fall into Disrepair

Professional owners do not buy a home in order to let it deteriorate. Their model works only if the property remains rentable, repairs are predictable, and vacancy is limited.

This is already evident at acquisition. The Urban Institute cites the annual reports of major SFR providers: Invitation Homes spent approximately $39,000 per home on initial renovations in 2020. American Homes 4 Rent typically estimated renovation costs of $15,000 to $30,000 for traditionally acquired homes.

This is not proof that every institutional landlord performs well. Renovation at acquisition is no substitute for reliable ongoing maintenance. Fees, response times, repair quality, and tenant communication remain critical areas of scrutiny.

Larger providers have a structural advantage: in-house processes, better purchasing terms, recurring contractors, and often 24/7 emergency response. Smaller landlords, however, may be more personal and able to make individual decisions faster.

The myth is therefore too broad. Institutional owners do not systematically allow homes to deteriorate. But professional ownership alone does not guarantee a good tenant experience.

Myth 7: Institutional Investors Reduce the Homeownership Rate

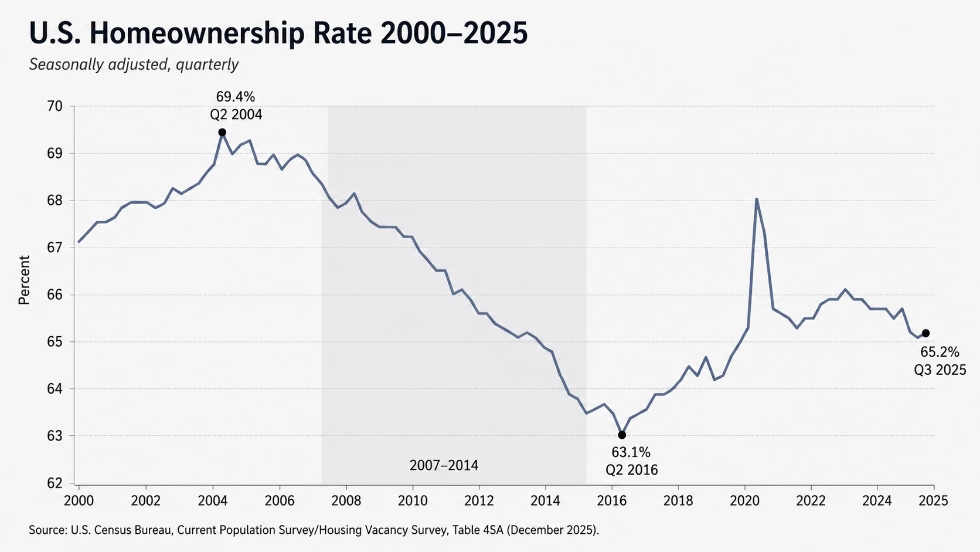

The homeownership rate tells a different story from the political slogan. It peaked in the United States at 69.2 percent in the second quarter of 2004—at the height of the credit and housing bubble. After the bubble burst, foreclosures, tighter lending standards, and the withdrawal of many households from the ownership market caused the rate to fall to 62.9 percent by the second quarter of 2016.

It has since recovered. In 2023, it reached 66.0 percent at times; in the third quarter of 2025, it stood at 65.3 percent. By comparison, Germany’s homeownership rate in 2025 is around 47 percent, well below the U.S. level. The current rate is therefore clearly below the bubble peak, but well above the post-financial-crisis low. This is shown by data from the U.S. Census Bureau and FRED.

The intervening period matters. As the for-sale market recovered after 2016, many previously rented single-family homes returned to owner-occupation. John Burns Research and Consulting describes how smaller investors sold homes at a profit and the stock of single-family rental homes declined.

More recent pressure on homeownership has other main drivers: high prices, higher mortgage rates, tighter financing, and insufficient down-payment capital. Institutional investors can play a role locally. They do not, however, explain the trajectory of the national homeownership rate.

The balanced conclusion: The United States has not experienced a steady slide into a housing market dominated by institutional landlords. The homeownership rate has been shaped more by credit cycles, interest rates, and affordability than by institutional SFR buyers.

Myth 8: Institutional Investors Are Bad Landlords

The quality of a landlord is not determined by the size of the owner. It is determined by response times, repair quality, fees, clarity of leases, and the treatment of tenants.

Institutional owners have structural advantages in these areas: professional management, standardized processes, digital maintenance systems, recurring service providers, and emergency response structures. The Urban Institute wrote as early as 2017 that there was no robust evidence that institutional investors were inherently worse landlords than mom-and-pop providers.

That does not mean scale automatically produces quality. Particularly at large platforms, fees, rent adjustments, repair practices, and eviction filings must be scrutinized closely. Brookings points to evidence that institutional owners in certain markets may raise rents faster and file eviction actions more frequently than smaller landlords.

Low tenant turnover is not unambiguous proof of satisfaction either. It may indicate good property management. It may also show that buying is too expensive and renters have few attractive alternatives.

The balanced conclusion: Institutional landlords are not automatically worse. Nor are they automatically better. What matters is operating practice—and it must be measured by repairs, transparency, fees, and tenant retention.

Myth 9: Institutional Landlords Raise Rents More Aggressively

Rents do not rise because an owner is institutional. They rise primarily where demand, incomes, and household formation grow faster than the available housing supply.

That does not mean institutional owners play no role. The 2024 GAO report found indications that institutional investors may have contributed to higher home prices and rents during certain periods. At the same time, the report emphasizes that the evidence remains limited and that studies are difficult to compare because they use different definitions.

The proper conclusion is therefore not that institutions never raise rents. It is that they are not automatically the main driver. Joshua Coven reaches a differentiated conclusion in his study: Institutional investors increased rental supply and reduced rents on net, while simultaneously reducing homeownership.

Here too, the local market matters. In tight locations, high concentration, fee models, and aggressive rent increases can burden tenants. Brookings therefore rightly points to the need for better data, clear tenant protections, and greater transparency.

The balanced conclusion: Institutional landlords can raise rents and may have problematic effects in individual markets. Broader rent growth, however, is explained primarily by supply, demand, and local market power—not by ownership structure alone.

Myth 10: In Markets Such as Atlanta, Institutional Investors Are Buying Everything

Markets such as Atlanta are the strongest challenge to national averages.

Two central claims are made here:

- Home prices: “In markets favored by institutions, such as Atlanta, home prices rise faster because institutions drive prices higher.”

- Rents: “In markets with significant institutional ownership, such as Atlanta, rents rise faster because institutions push them higher.”

Both claims deserve scrutiny. Neither is absurd. But they are often discussed using the wrong denominator.

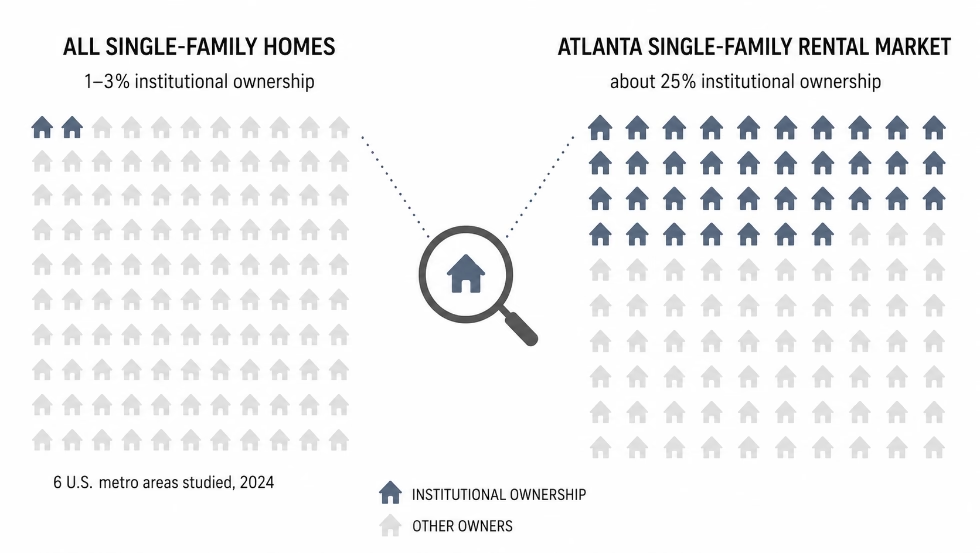

Across the entire housing market, the institutional share remains low. The GAO found institutional shares ranging from less than 1 percent to 3 percent of all single-family homes in six metropolitan areas studied. That is not enough to control an entire metro housing market or explain its price trajectory on its own.

The picture is different in the single-family rental segment. Institutional owners can hold significantly larger shares there. In Atlanta, institutional ownership was most recently reported at around 25 percent of the single-family rental market. That does not mean institutions are “buying up Atlanta.” It means they are large enough in the single-family rental submarket to warrant closer scrutiny. This is shown by the NLIHC summary of the GAO report.

This makes the core point visible: Institutional investors are too small a share of the overall housing stock to control the entire market. In the SFR segment and in individual submarkets, however, they can be material—for purchase prices, rental terms, fees, or eviction practices.

This concentration can affect purchase prices. Joshua Coven finds measurable price effects from institutional purchases in the most affected markets. That does not mean institutions determine prices for an entire market. It means they can move prices in concentrated submarkets.

The picture for rents is less clear. Coven also concludes that institutional entry increased rental supply and reduced rents on net. That is economically plausible: Purchases can support acquisition prices in tight submarkets, while additional or more efficiently operated rental supply can ease rental pressure.

The balanced conclusion is therefore: Atlanta does not demonstrate control over the entire housing market. It does show why the SFR submarket matters. Institutional owners can be relevant there without being the sole cause of high prices or rents.

Myth 11: Institutional Investors Provide No Public Benefit

This claim is also too absolute. Institutional investors do not solve the structural problems of the U.S. housing market—nor is that their role. They can, however, perform functions that are often harder to organize in a fragmented ownership market: They bring liquidity to tight markets, can professionally rehabilitate homes in serious need of repair, make certain locations accessible to renters, and increasingly create new supply.

- Renovation capacity: Large SFR platforms have the capital, contractor networks, and operating processes to renovate, maintain, and return homes to the rental market. Using Progress Residential as an example, the Urban Institute shows that approximately 43,000 homes were renovated between 2021 and 2023, at an average cost of about $32,000 per property. Larger owners can often execute such work more cost-effectively and predictably than small renovation firms or individual private owners.

- Access: Single-family homes in strong school districts or fast-growing suburbs are unaffordable to buy for many households, but available to rent. Institutional SFR offerings can give these households access to locations that would otherwise be closed to them as owners. This is no substitute for homeownership. It does, however, broaden the housing options available to families that cannot access the mortgage market or consciously choose to rent.

- Additional supply: When institutional capital creates new units—by building entire communities specifically for rental rather than purchasing existing homes—it expands the rental market instead of merely transferring existing stock. The Urban Institute considers large investors capable in principle of expanding supply through build-to-rent. The decisive point, however, is that genuinely new units must be created rather than ownership merely changing hands.

- Tenant infrastructure: Larger owners can provide services that are often harder for small landlords to implement: clear lease summaries, digital maintenance processes, more flexible security-deposit models, acceptance of Housing Choice Vouchers, or reporting rent payments to credit bureaus. None of this is automatic. It is a standard against which professional providers should be measured.

At the same time, the criticism remains justified. Public benefit does not arise from scale alone. Fees, rent adjustments, repair quality, eviction practices, and local concentration must be examined. The GAO report therefore offers no simple exoneration: Studies identify possible effects on prices and rents, but also stabilization after the financial crisis; the evidence on tenants and homeownership opportunities remains limited.

The balanced conclusion: Institutional investors do not automatically improve the housing market. But neither are they without public benefit. What matters is whether their capital actually creates liquidity, improves the housing stock, expands supply, and delivers measurably better standards for tenants.

The Eleven Myths at a Glance

| No. | Claim | Verdict | What the Data Shows |

|---|---|---|---|

| 1 | Institutional investors buy 25 percent of all homes. | False | The figure combines small landlords, flippers, LLCs, and institutional platforms. Institutional buyers account for only a small share of transactions nationwide. |

| 2 | Without institutional buyers, SFR renters would become homeowners. | Mostly false | Insufficient down-payment capital, creditworthiness, high interest rates, and monthly costs frequently prevent a purchase. |

| 3 | Institutional buyers drive home prices higher. | Partly true | Price effects are measurable in concentrated submarkets. Nationwide, however, institutional investors are not the main driver. |

| 4 | Institutional buyers displace families with cash offers. | Oversimplified | Not every cash offer comes from an institutional investor. Competition exists, but a systematic pattern of displacement has not been established. |

| 5 | Institutions primarily buy up affordable starter homes. | Partly true | Many purchased homes are inexpensive because they need repairs and are harder to finance. Direct competition with first-time buyers nevertheless exists. |

| 6 | Institutional owners let homes fall into disrepair. | Not supported as a general claim | Large providers often invest substantial amounts in renovation. Professional scale, however, does not guarantee reliable ongoing maintenance. |

| 7 | Institutional investors reduce the homeownership rate. | Mostly false | The national homeownership rate is shaped more by credit cycles, prices, interest rates, and access to financing. |

| 8 | Institutional owners are bad landlords. | Not supported as a general claim | Large providers have professional structures, but may still perform poorly on fees, repairs, and eviction practices. |

| 9 | Institutional landlords raise rents more aggressively. | Unclear and market-specific | Institutional owners can influence rents and fees locally. Broader rent growth primarily follows supply and demand. |

| 10 | In markets such as Atlanta, institutions are buying everything. | False—with a local element of truth | Their share of the overall market remains small. In the rented single-family segment of individual submarkets, however, concentration can be substantial. |

| 11 | Institutional investors provide no public benefit. | False | They can renovate existing stock, create additional supply, and build professional tenant-service structures. The benefit, however, does not arise automatically. |

The Real Problem Is Not Wall Street. It Is Scarcity.

After eleven myths, a sober conclusion remains: Institutional investors are neither the main cause of America’s housing problems nor automatically their solution.

The image of institutional investors as “locusts” is understandable because it captures a broader unease: large pools of capital, standardized processes, remote owners, and rising rents. But it is not sufficient as analysis. It does not explain why too little housing is built, why financing is unaffordable for many households, or why local markets function so differently.

Their share of the overall housing market is too small to explain high prices, poor affordability, or declining homeownership opportunities on its own. In individual SFR submarkets, institutional owners can nevertheless be relevant—particularly where holdings are locally concentrated, lease terms are standardized, and fees or eviction practices become prominent.

The better response therefore lies not in simple bans, but in clearer standards.

- More supply: Not merely more capital, but more buildable land, faster permitting, more new construction, and more housing types between apartments and detached single-family homes.

- Better data: Anyone discussing institutional investors must distinguish among small landlords, local LLCs, flippers, iBuyers, build-to-rent developers, and large SFR platforms. Without that distinction, policy responses target the wrong categories.

- Better standards: Institutional capital should be judged by whether it improves the housing stock, leases transparently, discloses fees, organizes repairs reliably, and treats tenants fairly. Scale alone is not a measure of quality. Professionalization must be evident in day-to-day operations.

This is the constructive perspective: Institutional investors should not be made the scapegoat for structural scarcity. But neither should they be allowed to hide behind market logic.

The U.S. housing market needs more supply, greater transparency, and owners who prove responsibility through their operations. Not in the narrative. In the properties.