Many portfolios are more broadly spread than they are genuinely diversified.

They hold equities, bonds, real estate, bank deposits, life insurance policies, pension commitments, and participations. On paper, this looks like structure. Multiple pillars. Professional wealth allocation.

But the real question begins one level deeper:

Which system does this wealth depend on?

The same currency area. The same banks. The same legal framework. The same tax rules. The same political decisions. Often the same economic trajectory as well.

This is precisely where it becomes uncomfortable for European investors. A portfolio can appear solidly diversified at first glance while being, in reality, heavily concentrated — not in a single stock, not in a single sector, not in a single property, but in a single system.

This is not an academic distinction. It is one of the central questions of modern wealth structuring: what does diversification mean when almost all assets are subject to the same legal, fiscal, and monetary framework?

Control Over Assets: The Underestimated Dimension of Wealth

Diversification is commonly understood as a question of asset classes. That is not wrong. But it is incomplete. Wealth consists not only of titles of ownership, custody positions, and contractual claims. It also consists of the practical ability to exercise control over those assets at the moment it matters.

The Jacques Baud Case: An Isolated Incident — But Not an Irrelevant One

The Jacques Baud case illustrates why this question is not merely theoretical. Baud, a former Swiss military intelligence officer, was placed on a European Union sanctions list in late 2025. Swiss media reported that his accounts and cards at UBS were blocked or restricted to essential transactions only. Particularly noteworthy: Switzerland had not, according to these reports, adopted the underlying EU sanctions in the same form.

One should not construct a grand theory of systemic failure from a single case. That would be irresponsible. But one should not dismiss it either. Because it reveals something that receives too little attention in many wealth plans: wealth is not only a question of ownership. It is also a question of control.

A bank deposit, a securities portfolio, an insurance policy, or a participation can exist on the balance sheet. What matters is whether you can actually exercise control over it at the moment it counts.

Taking diversification seriously therefore means asking not only: which asset classes am I invested in? But also: in which legal jurisdictions, through which institutions, and under which political access conditions does my wealth reside?

Cyprus 2013: When Bank Deposits Became Risk Capital

Cyprus was not a theoretical scenario. It was a real stress test within the eurozone.

In March 2013, the two largest banks in the country — Laiki Bank and Bank of Cyprus — were restructured. Deposits up to EUR 100,000 remained protected in principle. Deposits above that threshold, however, were no longer treated as ordinary bank balances.

They were partly drawn upon to recapitalise the banks. At Bank of Cyprus, portions of unsecured deposits were converted into equity; the bank itself later stated that the share of affected deposits converted into shares under the bail-in amounted to a total of 47.5 percent.

For high-net-worth investors, the Cypriot particulars are not the decisive point. The principle is: A bank deposit is not a safe. It is a claim against a bank. If that bank enters a resolution regime, what appeared to be available liquidity can suddenly become tied-up, written-down, or converted capital.

The same caveat applies: no simple panic thesis should be drawn from Cyprus. Not every bank deposit is at risk. Not every European bank is a Cyprus scenario. But Cyprus demonstrated that effective control and the sense of ownership can diverge. If you hold EUR 500,000 in an account, that feels liquid. Legally and economically, however, above the deposit guarantee threshold you are a creditor of the bank.

This is not an argument against bank deposits. It is an argument against complacency.

Taking diversification seriously therefore means it is not enough to distribute wealth across different asset classes. You must also ask: where is my capital held? Under which resolution law? In which currency area? At which institutions? Which parts of my wealth would genuinely be accessible in a systemic crisis?

If you do not ask this question, you are confusing allocation with protection. This is not a minor distinction. It determines whether a portfolio merely looks orderly — or is genuinely more resilient.

From Exceptional Case to Legal Framework

What many at the time regarded as a Cypriot exception later became part of a European resolution framework. The Bank Recovery and Resolution Directive was adopted in 2014. In Germany, the Sanierungs- und Abwicklungsgesetz (Bank Recovery and Resolution Act) entered into force on 1 January 2015.

The deposit guarantee up to EUR 100,000 remains protected. Deposits above that threshold, however, are not ring-fenced assets — they are part of a bank’s liability structure. In a resolution scenario, depending on creditor ranking and resolution decisions, they may be subject to a bail-in.

Cyprus was therefore not merely an exception. It was an early European instance of a logic that was subsequently codified more systematically in bank resolution law. The Deutsche Bundesbank describes the bail-in explicitly as an instrument through which a bank’s liabilities can be written down in whole or in part, or converted into common equity tier 1 capital.

What Diversification Was Originally Meant to Do

Diversification is not an invention of the financial industry. It is an old commercial insight: the wisdom of not putting all eggs in one basket predates financial mathematics.

Harry Markowitz did not invent this insight in 1952 — he formalised it. In his paper “Portfolio Selection,” he demonstrated that a portfolio of multiple assets can carry lower risk at the same expected return, provided those assets are not perfectly correlated. For this work, Markowitz received the Nobel Prize in Economic Sciences in 1990, jointly with Merton Miller and William Sharpe. The Nobel Foundation describes his theory explicitly as the foundation of modern portfolio selection.

The core idea remains valid. A portfolio consisting of a single stock is more vulnerable than one holding many. A wealth structure concentrated in one industry is more exposed than one spread across multiple sectors. An investor holding exclusively real estate carries different concentration risks than one who also holds liquid assets, business participations, and securities.

Classical diversification reduces idiosyncratic risk. It protects against the wrong company, the wrong sector, the wrong property, or the wrong entry timing. But it does not answer every question.

Markowitz conceptualised diversification within a functioning market and legal framework. His theory asks: how do assets behave relative to one another? It does not ask first: under which currency area, which legal framework, and under which political access conditions do these assets reside?

That is precisely where the blind spot of many portfolios begins today.

When equities, bonds, bank deposits, insurance policies, real estate, and pension entitlements are all subject to the same currency area, the same institutions, and the same political decisions, a concentration emerges that is barely visible in standard portfolio overviews. The asset classes differ. The systemic framework is the same.

That is the difference between apparent diversification and genuine international wealth diversification.

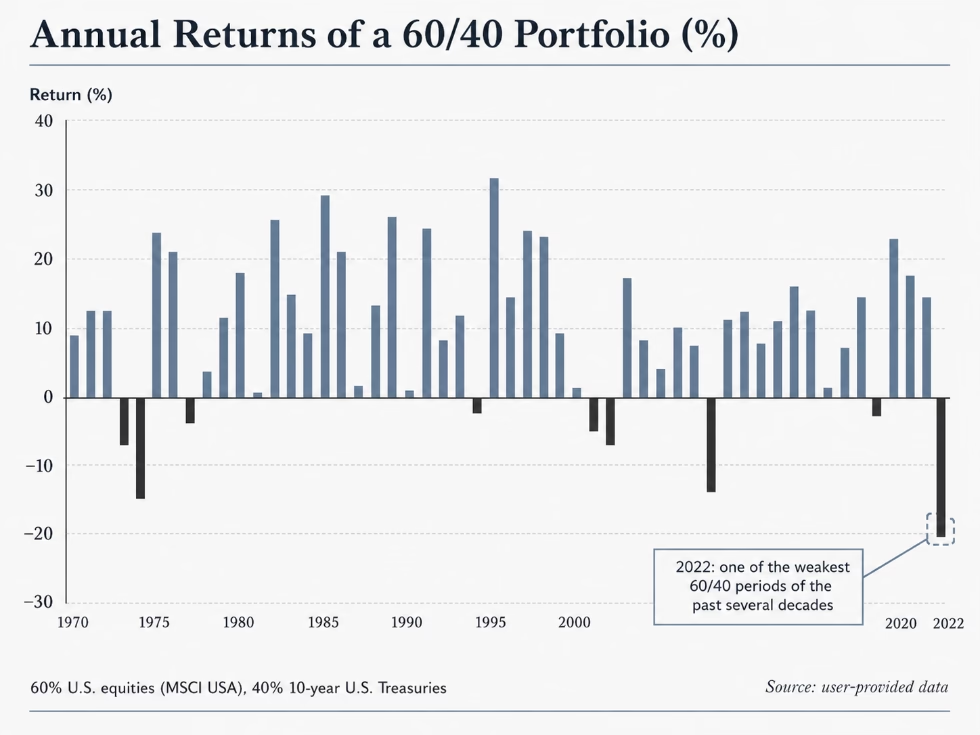

2022 demonstrated how quickly familiar correlations can break down. The classic 60/40 portfolio of equities and bonds had long been regarded as a robust standard architecture. But when inflation and rising interest rates simultaneously compressed equity valuations and bond prices, both sides of the portfolio fell together. MSCI described this period as one of the weakest for the 60/40 strategy in decades.

The lesson is not that classical diversification is wrong. That would be too simple.

The lesson is more precise: diversification across asset classes is necessary, but not sufficient. To protect wealth over the long term, one must also examine the deeper dependencies: currency, legal framework, regulation, taxation, political access conditions, and the real economy from which cash flows are generated.

Only there does diversification begin that truly deserves the name.

System Risk Appears in No Tidy Portfolio Overview

Most portfolio overviews show asset classes. Equities. Bonds. Real estate. Liquidity. Participations. Perhaps commodities or private equity.

What they rarely show is the common framework underlying all of them.

The idiosyncratic risk of an individual investment can be managed through diversification reasonably well. A company can fail. A sector can come under pressure. A real estate market can overheat. Classical diversification helps: more companies, more sectors, more properties, more maturities, more tenants.

System risk operates at a deeper level.

It does not concern the individual investment, but the order within which that investment exists: currency, legal system, banking structure, capital flows, property rights protection, tax policy, regulation, and political access conditions.

If you are broadly diversified within the same system, you hold many positions. But not necessarily many independent risks.

This was precisely illustrated in 2022 by Russian assets. An investor there could hold government bonds, equities, real estate, and bank deposits. By conventional definition, that was diversified. In reality, everything depended on a shared political and geopolitical framework. When that framework broke, diversification within the system provided only limited protection.

A different example, closer to home and less dramatic: Greece in the summer of 2015. Bank customers were restricted to limited cash withdrawals; outbound transfers were curtailed. No one automatically lost ownership of their assets. But effective control was temporarily suspended. This occurred within the eurozone, on the basis of a valid legal framework, without a bail-in and without a conventional bank insolvency.

Sovereign wealth managers are now asking this question afresh. Following the freezing of Russian central bank reserves in 2022, gold became more attractive as a reserve asset again, precisely because it carries no claim against a Western custodian. This offers no perfect protection and no simple lesson. But it demonstrates that even central banks are now thinking more carefully about access, custody, and counterparty risk.

The point is not Russia. The point is the logic.

A portfolio can be formally diversified and yet depend on a single underlying assumption: that the legal framework, the currency area, and the institutions upon which it rests will remain stable and will not restrict access to assets.

This assumption may well be correct. But it should not remain unexamined.

Taking diversification seriously therefore means asking not only how many asset classes you hold. You must ask how many distinct systems genuinely underpin your wealth.

Only then does allocation become a robust risk concept.

How Much of Your Wealth Depends on the Same System?

The decisive question is simple. The answer often is not.

What share of your wealth depends on the eurozone system?

Not just your bank deposits. Also equities, bonds, life insurance policies, pension entitlements, occupational pension schemes, real estate, business participations, and future statutory pension claims.

If your answer exceeds sixty percent, you should take note. Not because sixty percent is a magic threshold. But because beyond that point, diversification very quickly becomes concentration.

In conversations with high-net-worth investors from Germany and Austria, we frequently encounter significantly higher figures. Not sixty percent. More commonly eighty or ninety.

At that point, we are no longer speaking of genuine international wealth diversification. Your wealth is, at its core, dependent on one large shared assumption: that the same currency area, the same legal framework, the same institutions, and the same political decisions will remain viable in the long term.

You may hold equities, real estate, liquid assets, and business participations. That appears broad. But if almost everything is located in Europe, denominated in euros, subject to European tax and welfare state frameworks, and affected by the same political decisions, a concentration emerges that is barely visible in standard wealth overviews.

A primary residence in Munich, a rental apartment in Berlin, a portfolio of European index funds, a German life insurance policy, and an occupational pension scheme may appear to be distinct components of a well-structured wealth plan. At a deeper level, however, they share the same institutional signature: the same currency area, the same political order, similar fiscal burdens, similar regulatory risks.

This is not a criticism.

This structure was rational for decades. Europe was stable. Germany was regarded as reliable. The euro was taken as a given by many investors. Domestic real estate felt safer than participations in a foreign legal environment.

But past stability is no guarantee of future conditions.

If eighty or ninety percent of your wealth depends on the same system, that is not automatically wrong. But it is not genuine international wealth diversification either.

It is one large shared assumption. That assumption may be correct. It should simply not remain the unconscious foundation of your entire wealth structure.

Decoupling as a Strategy

The critical step is not to avoid risk. That would be impossible.

The critical step is to decouple risks from one another.

If you want to diversify your wealth internationally, it is not enough to hold different asset classes. What matters is whether those assets are exposed to different systems: different currency areas, different legal frameworks, different regulatory regimes, different tax logics, and different economic trajectories.

This decoupling can begin geographically.

A residential property in a high-growth US market is subject to different risks than a pre-war apartment building in Berlin. Both are real estate. Both can generate rental income. Both require sound management, disciplined financing, and consistent maintenance. But they are not governed by the same tenancy law, the same energy policy, the same tax logic, or the same demographic trajectory.

That is precisely why they do not represent the same risk.

Decoupling can also concern jurisdiction. Assets held in US structures are subject to different legal rules than assets held in a German GmbH, a European securities portfolio, or a Swiss bank account. This does not mean: no risk.

It means: a different risk. For European investors, this is precisely the decisive point — because genuine diversification does not arise from the absence of risk, but from the absence of correlation.

The nature of the asset also matters. Productive real assets generating ongoing cash flows behave differently in stress scenarios than claims whose value depends primarily on confidence in a bank, a sovereign, an insurer, or a pension system.

Decoupling is not risk avoidance.

The objective is not to hold no risk. The objective is to hold different risks — risks that do not materialise simultaneously, do not originate from the same source, and do not depend on the same political decisions.

Only then does international wealth diversification become more than a visually appealing chart in a wealth report.

The Honest Answer to a Common Question

When European investors ask why they should allocate capital to US Sunbelt real estate, the honest answer is: not for the return alone.

Return matters. But return without an understanding of risk is just a number on paper.

The real point is a different risk profile.

A professionally structured multifamily investment in Florida is not exposed to the eurozone system. It is not subject to German tenancy law, European energy efficiency mandates, German energy policy, or the same fiscal logic that will increasingly preoccupy European property owners in the years ahead.

It operates within a different system.

This does not mean: no regulation. Nor does it mean: no risks. US real estate carries its own risks: financing costs, insurance, natural events, local market cycles, asset management quality, maintenance, and exit liquidity.

But that is precisely the point: they are different risks.

Florida is not an unregulated market. But many of the core aspects of residential tenancy law are governed at the state level, precluding local deviations. Florida Statute § 83.425 establishes this preemption explicitly for residential tenancies and the landlord-tenant relationship.

For investors, this means: the regulatory environment is not risk-free, but it is clearer and less fragmented than in many European residential markets.

There is also a meaningful demographic tailwind. While many European markets are contending with ageing populations, regulatory burdens, and fiscal pressures, many Sunbelt regions have benefited for years from population inflows, household formation, and economic momentum that is independent of EU fiscal policy.

This is precisely where Whitestone Capital operates. Not as a product promise, but as a structural proposition: providing European capital with access to a real estate market governed by different monetary, legal, regulatory, and growth dynamics.

That is decoupling. Not perfect safety. Not protection against every crisis. But a different risk profile from the one with which European wealth structures are typically already heavily loaded.

When the system in which the majority of your wealth resides comes under serious pressure, one simple question arises:

What remains viable independently of that?

If you do not have a convincing answer to that question, there is no need for panic. But there is a need for a better wealth structure.